Life after the Budget

Attractive valuations revive FII interest but for momentum to sustain, corporate profitability is key

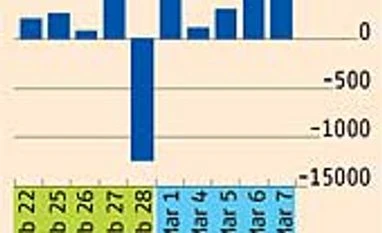

Malini Bhupta Mumbai Since January this year, foreign institutional investors have pumped in over $8 billion (over Rs 43,000 crore) into Indian equities, of which $4.6 billion came in February. And had the Budget lived up to its "dream" expectations, the market would have seen a rush of dollars. Despite the disappointment with the Budget, foreign institutional investors (FIIs) remain overweight on India. This is reflected in the benchmark indices, too. The Nifty is up 2.57 per cent after the Budget and the Sensex is up 2.77 per cent.

The weak macro-economic numbers notwithstanding, global fund managers continue to be optimistic on Indian equities. In a recent report, JP Morgan says the number of fund managers with "overweight" position on India in the emerging market portfolio is at a multi-year high.

Strategists say that aggregate futures and options open interest largely remained unchanged over the past one month, even though FIIs were net sellers in the futures market over the last one week. All that has happened is that the mixed macro-economic data has made investors a little cautious, which is why volumes remain thin in the cash market and open interest in stock futures reduced but increased for index futures.

While this explains the moderate correction in the market after the Budget, many have been caught unaware by the sharp uptick in stock prices this week. So, is this a dead cat bounce and are capital flows to India likely to moderate? If valuations are anything to go by, then the current uptick is more about attractive valuations and cherry picking than anything else. According to the valuation model of Credit Suisse, Indian markets have joined the club of the cheapest four markets, replacing MSCI Hong Kong and Australia. This is the 15th time that this has happened since 2000 when Credit Suisse introduced this valuation model and 13 out of the past 14 times MSCI India outperformed MSCI Asia-ex Japan after 12 months. India's premium to the region has dropped to four per cent, similar to December 31, 2011, says the Credit Suisse report.

Valuations can be a good trigger for buying, but it's not a sustainable trigger. Ultimately, markets need growth, which is unlikely to revive in the new fiscal. Even though the improved market conditions, on the back of portfolio flows, have made fund-raising easier for companies and foreign direct investments have largely remained stable, analysts are now worried about deceleration in profit growth after a sharp slowdown in sales. For momentum to sustain in the markets, the real economy needs to improve.

According to Morgan Stanley, the trend in exports and government efforts to revive investment will be the two anchors to growth sentiment. "Of the two, we think private investment will be the more important factor to support aggregate demand and GDP growth as the government stays on the path of fiscal consolidation."

"Life after the Budget")