Subsidiary downgrade might not impact GMR Infra's fortunes

Despite large levels of debt, what augurs well is the significant recovery in operations in the first quarter of FY16

S Hamsini Amritha Mumbai Rating agency CARE downgraded the credit facilities of GMR Hyderabad Vijayawada Expressway Private Limited, a 90 per cent subsidiary of GMR Infrastructure, on Wednesday. This might have led the GMR Infra stock to shed nearly three per cent to end at Rs 13.11 on Thursday, a day the broader markets were marginally up.

CARE reduced its rating from BBB minus on long-term facilities and A3 on short-term facilities to D, indicating these facilities are in default or expected to be in default in future. Although the highways division accounts for only eight per cent of the total capital employed by GMR Infra as on March 31, 2015, the downgrade comes at a time when the company has large loan outstanding and high interest costs. The company's consolidated loans stood at Rs 47,738 crore at the end of FY15, taking the debt-equity ratio to 5.57 times (vs 5.44 times in FY14 according to data in Capitaline).

Despite these levels of debt, what augurs well is the significant recovery in operations in the first quarter of FY16. GMR Infra closed the quarter posting profit before interest, depreciation and tax of Rs 1,003 crore versus Rs 660 crore in the year-ago period. Operating profits were primarily driven by 13 per cent increase in passenger growth in Delhi and Hyderabad airports, improved operations in the energy division and higher traffic growth in the highways division.

However, interest costs inched up nine per cent to Rs 906 crore and along with depreciation charge of Rs 454 crore, led to a net loss of Rs 429 crore versus Rs 576 crore in the first quarter of FY15, adjusted for one-offs. While the operational improvement is positive, CARE's recent downgrade might weigh on sentiments in the near-term.

The ongoing delay in servicing debt obligations and persistent cash loss on account of lower-than-anticipated toll revenues have been cited as reasons for downgrade by CARE. This also means revenues might remain under pressure for some time led by the subdued economic environment, which typically has a bearing on road traffic.

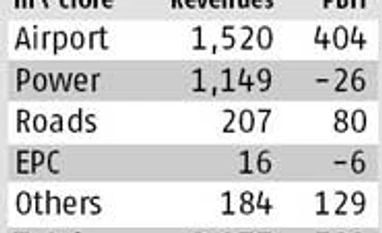

Although the highways business’ revenue contribution is only seven per cent to GMR Infra’s total revenues, it still holds the key for the company. While total revenues of the company grew 6.3 per cent in the first quarter of FY16, that of the highway divisions expanded 13.3 per cent. Likewise, it is also the highest contributor to operating margins.

The company's consolidated earnings before interest, taxes, depreciation and amortisation margins stood at 36 per cent for the June quarter, while that of the highway division is 70 per cent —ahead of the airport business (56 per cent). While the Street will closely watch the developments in the business, the improving show by the airports business and the relief provided by the government in the energy business (subsidy on imported gas leading to better utilisation levels of power plants) are bigger positives. For instance, the airport business continues to see healthy growth in traffic and with 50 per cent margins, it made a net profit of Rs 120 crore in the June quarter.

After scaling to its all-time intra-day low of Rs 9.58 earlier this month, the stock is up 37 per cent at Rs 13.11 currently. Although the first quarter of FY16 was positive for GMR, the gains could get bigger if the company is able to shrink its debt meaningfully and operational performance improves further. Meanwhile, of the seven analysts polled by Bloomberg, four have ‘buy’ recommendation, while two recommend ‘hold’ and one ‘sell’.

"Subsidiary downgrade might not impact GMR Infra's fortunes")