Currently, valuations within the equity markets are at a premium to long-term averages, more so within the mid-and small-cap segments. The trailing 12-month price-to-earnings ratio of the BSE Sensitive Index, or Sensex, is currently at 22.7, higher than its five- and 10-year averages of 19 and 19.3 per cent, respectively. In such a scenario, there is always the risk of a market correction. One way for investors to guard against it is through opting for style diversification within their portfolios. If they have been investing only in growth funds so far, they should now also opt for value-oriented funds, such as dividend yield funds.

These funds invest in stocks that offer a certain minimum level of dividend yield — say, 3 per cent or more. Typically, these stocks tend to be of mature companies with strong balance sheets. They have minimal capital requirements and are able to generate regular free cash flows. Dividend yield funds’ mandate prevents them from investing in younger, fast-growing and cash-hungry stocks.

Dividend yield funds tend to outperform growth funds in falling markets. "Younger, growth-oriented companies need to raise capital for growth. This becomes difficult when the economy and the markets are not doing well," says Anand Shah, deputy chief executive officer and chief investment officer, BNP Paribas Mutual Fund. Dividend yield funds tend to be more resilient at such times as the stocks in their portfolios don't need to raise capital.

The dividend paid out by these stocks also places a barrier or floor, which stems the decline in their stock price. "As prices fall, the dividend yield of these stocks rises, hence investors tend to flock to such stocks in weak market conditions," says Nikhil Banerjee, co-founder, MintWalk.

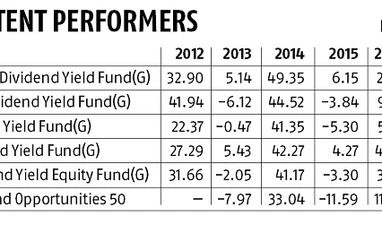

Many dividend yield funds in India have managed to create an attractive track record (see table), which is another reason why you should consider allocating some part of your portfolio to them.

However, remember that when the markets are rallying strongly, dividend yield funds may underperform growth funds in those phases.

These funds can be part of an investor's portfolio in several circumstances. Shah suggests investors should always have a 70% allocation to growth funds and 30% to value-oriented funds, including dividend yield funds. "This will make the portfolio more stable," he says.

A quality dividend yield fund would also fit well into a conservative equity investor's portfolio. Investors with a dynamic approach, that is, those who change their portfolios based on market outlook, may also take exposure to these funds now. "If the markets fall from their current levels, these investors will be well-positioned to deal with the volatility," says Banerjee.

Retirees, who need regular dividend income, may also consider dividend yield funds. Such investors should, however, look at the dividend payment track record of the fund they invest in. BNP Paribas Dividend Yield Fund, for instance, has established a track record of having paid dividends continuously for the past 51 months. The income that you need to generate to meet your essential expenditure should come out of fixed-income instruments, but for meeting your discretionary expenses you may depend on these funds (since they are not obliged to always pay a dividend). Your investment horizon in these funds should exceed five years.

"Here's how to make your investment portfolio more resilient")