Until a decade ago, watches were Titan’s bread and butter, accounting for about half its revenues. But still, Titan, for all its appeal, wasn’t among the top-ranking companies in market value for the Tata group. Even though Titan is now India’s largest-selling watch brand, it is the jewellery business which has changed the company’s fortunes in the past few years.

Monday’s 19 per cent gain in Titan’s stock price, which adds to the strong rally seen this calendar year, made Titan the third most-valuable company in the Tata group. This, itself, is a statement of how important the company has emerged. The Titan stock surged past Tata Steel and is now behind the group’s flagship Tata Consultancy Services (TCS) and Tata Motors in market value.

Incidentally, Tata Steel is one of Tata’s oldest businesses and generates revenues five times larger than that of Titan. Yet, with Monday’s market cap of Rs 69,651 crore, Titan surpassed Tata Steel’s Rs 68,834 crore of market cap.

Titan’s promotion to this league, in a way, reiterates investors’ preference for consumer-oriented stocks, particularly those which are successfully withstanding the test of formalisation. In fact, ace investor Rakesh Jhunjhunwala was among the early ones to identify the potential in Titan.

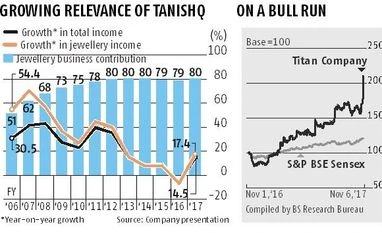

The growing relevance of Titan’s gold business has changed things for the best. Even for the September quarter’s (Q2’s) stellar performance, all credit went to Titan’s jewellery business, which exceeded expectations.

While Q2 is usually propped up by festive and marriage season demand, analysts anticipated the current year’s Q2 would be relatively subdued due to Prevention of Money Laundering Act (PMLA) becoming applicable for jewellers. Accordingly, jewellers were required to furnish detail of their customer’s permanent account number (PAN) for purchases exceeding Rs 50,000. Notwithstanding this, the jewellery division’s revenues rose 36 per cent to Rs 2,711 crore, lifting Titan’s Q2 revenues by 30 per cent to Rs 3,376 crore.

What also lent some support in Q2 was that other segments — watches and eyewear — also performed a tad above expectations, posting revenue growth of nine per cent and 3.5 per cent, respectively, on the back of festive demand. While the eyewear segment’s realisations remain muted (1.4 per cent; Ebit margin in Q2), that of watches expanded to 16 per cent versus 12.3 per cent a year ago. Again, the management is cautious if the margin improvement is sustainable as the product mix could alter in the coming months.

Therefore, with its ancillary businesses not adding up much, gold and diamond (jewellery) now accounting for 80 per cent of Titan’s overall revenues will remain the key growth driver in the medium- to long-term. What’s more, with the key trigger of informal sector demand folding into the formal channels playing out better than anticipated especially in case of Titan, most analysts including those at CLSA feel the company is a strong consumption play on formalisation of the jewellery sector. In this backdrop, it may be time to rename Titan to Tanishq, say analysts.

Interestingly, if gold is sought after, irrespective of its price, the Titan stock, too, is in vogue irrespective of its valuations. Currently trading at 44x FY19 earnings, Titan is at a significant premium to most consumer stocks. Yet, analysts by and large remain bullish on the counter. Analysts at Bank of America-Merrill Lynch increased their earnings estimates by 16 per cent, 20 per cent and 24 per cent for FY18, FY19 and FY20 respectively factoring in faster than expected scale-up in the jewellery business along with higher margins. Those at Deutsche Bank have upped their FY17-19 earnings estimate by 17 per cent, and the target price from Rs 625 to Rs 900.

After all, winners aim for a gold medal and this optimism appears rightly placed.

"Jewellery helps Titan become third-most valuable Tata firm")