The mention of ICICI Bank might trigger caution, with three dismal quarters of results, in asset quality and earnings pressure. This explains why its stock hasn’t delivered as much yearly return as peers HDFC Bank or Axis Bank.

It appears a reversal in this is on the anvil. The value unlocking opportunities ahead are a major trigger for a re-rating in the near term. The Securities and Exchange Board of India’s (Sebi’s) approving the listing of its life insurance business took its stock up about two per cent on Wednesday. And, the business fundamentals, after bottoming in the March quarter, are recovering. Analysts believe earnings from here are on a path of recuperation and the worst could well be over.

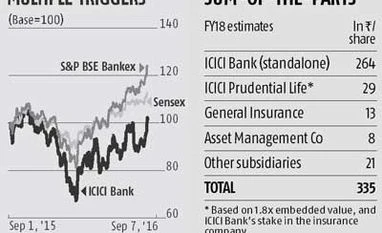

First on the most awaited Initial Public Offer (IPO) of its life insurance arm, ICICI Prudential Life Insurance (I-Pru Life). With Sebi's nod, the process should commence in a few weeks. Going by the draft prospectus, the bank is likely to pare 10-12 per cent stake in I-Pru Life, through an Offer for Sale (OFS). The bank now holds 68 per cent stake in the arm. Reports indicate the IPO might raise Rs 4,500–5,000 crore; since it is an OFS, the proceeds will accrue to the bank.

The other positive trigger is the valuation boost the bank's stock will see. According to analyst estimates, the valuation of I-Pru Life is likely to keep pace with the benchmark set by the recently concluded HDFC Life-Max Life transaction (3.8-4 times the embedded value). As I-Pru Life’s business is now valued at 1.6-1.8 times this much, the IPO offers significant potential for the stock to re-rate.

General insurance and housing finance are among the key non-core entities of the bank. Any possible value unlocking (part stake sale or IPO) in these could also prop the ICICI Bank stock.

The Street is starting to reward the stock for the manner in which ICICI Bank had disclosed its asset quality pain. As Siddharth Purohit of Angel Broking explains, “While the asset quality pain is not going to change drastically, the predictability of earnings has improved sharply for ICICI.” With better disclosure in place, Religare Institutional Research recently upgraded ICICI from ‘sell’ to ‘hold’. In their report, they highlight, “We prefer ICICI Bank over Axis Bank from a three-year perspective, as it has a clear edge on the asset quality front.”

It feels ICICI Bank has been more prudent in managing asset quality stress. “For the top two troubled sectors (iron & steel and power), ICICI Bank has prudently classified 32 per cent of stressed exposure as NPA (non-performing assets), whereas Axis Bank has classified just four per cent,” the report adds.

With this, analysts feel a large portion of incremental bad loan slippages should emerge largely from the June quarter’s watch list of Rs 38,700 crore for ICICI Bank. The bank has already made contingent provisions of Rs 3,600 crore to handle the probable NPAs (of which Rs 860 crore was used in this financial year's first quarter). Gains from the stake sale in I-Pru Life will provide further cushion in the event of additional write-offs or provisioning. All these should support earnings.

With these aspects in place, analysts feel a noteworthy re-rating for ICICI Bank’s stock doesn’t appear too far. Currently trading at 1.7 times the FY17 price to book value, its valuations are the lowest among larger private banks, quoting at 2.5 to four time the one-year forward book value.

"ICICI Bank stock ripe for re-rating: Analysts")