When an individual wants to leave a legacy for his grandchildren, usually, he buys a life insurance policy or invests in a fixed deposit in the name of the minor. Only a few focus on creating a legacy portfolio that can be passed to their children and grandchildren. Typically, the family wealth that the next generation inherits includes properties and what is left of the retirement corpus. But with a little planning, you can leave a much bigger corpus for the next generations.

Instead of investing a lump sum in the name of each child or grandchild individually, a person can create an investment portfolio by investing in a mix of asset classes. “An individual can choose simple long-term assets that don’t require a regular evaluation of the portfolio. As such portfolios will continue for decades, the compounding will ensure that you leave a meaningful corpus for the next generation,” says Malhar Majumder, a partner at wealth management firm Positive Vibes Consulting and Advisory.

If your portfolio grows at six per cent annually, an initial investment of Rs 1 million can become Rs 4.3 million in 25 years. At 8 per cent annual return, the portfolio will grow to Rs 6.8 million over the same period.

A trust for a larger corpus: A trust is the best vehicle for passing assets on to the next generation if they are significant. “It leaves no scope for disputes among beneficiaries, as is common in the case of a Will. It ring-fences assets. Lenders cannot attach assets that are placed in a trust,” says Arnav Pandya, certified financial planner

A trust, however, is a rigid structure. Once formed it’s difficult to change. Winding it up is cumbersome. You need to, therefore, be clear on the assets that you want to include in a trust, and the beneficiaries. You can write an investment policy statement that outlines the general investment goals, objectives, and describes the strategies that should be employed. You can take the help of a fee-only investment advisor who would charge anywhere between Rs 20,000 and Rs 45,000 as a one-time payment. To set up a trust, lawyers charge around Rs 25,000. Once floated, you will need to spend around Rs 15,000-20,000 annually to maintain it. The recurring cost includes compliance-related expenditure and chartered accountant's fee for maintaining the account and filing annual returns. “For those with limited assets, a Will can be sufficient,” says Suresh Sadagopan, founder, Ladder7 Financial Advisories.

Safety is the key objective: Most people start thinking about leaving a legacy in their fifties or after retirement. The aim is to pass on a meaningful corpus to the next generation. By then capital preservation has already become their primary focus. The investments that you make in a legacy portfolio need to be long-term and should align with the tenure of your goal. If you are 55, and your life expectancy is 85 years, your goal is 30 years away. An investor needs to choose products that do not require active management.

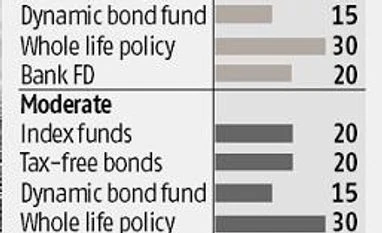

Building the portfolio: An actively-managed fund would require the investor to review it regularly, which may not be feasible for a senior citizen or someone approaching retirement. Investment advisors, therefore, suggest that index funds work out to be the best products for long-term passive investing. The investor, in this case, doesn’t need to worry about keeping a tab on the fund’s performance. Select an index fund that doesn’t invest in derivatives, has low tracking error historically, and whose expense ratio is low. Opt for a fund that invests either in the Nifty 50 or the S&P BSE Sensex.

You can also look at direct stocks, but be very selective and go for bluechip stocks from the Sensex or Nifty. Invest in companies that you think can remain bluechips even decades later, such as fast moving consumer goods giants like ITC and HUL, or government companies such as ONGC. The allocation to equities should be 15-25 per cent of the portfolio, depending on the individual’s risk appetite.

For the debt portion, which will be significant in the portfolio, opt for tax-free bonds from the secondary market that has a tenure of 20 or more years. In the current market, you can get tax-free bonds that would mature in 2034 and 2035 offering a yield-to-maturity of over 6 per cent. Dynamic bond funds also work best over the long term. These funds have given an average return of 7.84 per cent over the past 10 years. Allocate around 35 per cent combined to tax-free bonds and to dynamic bond funds. A small portion can be invested in long-tenured fixed deposits and even in the government of India’s savings (taxable) bond that yields 7.75 per cent return annually. For a long-term portfolio, investment in gold is essential. “Keep five-10 per cent in gold by investing in either sovereign gold bonds or gold exchange-traded funds,” says Pandya.

Whole life policies: Insurance companies have started to offer term plans that cover the policyholders for their entire life. These products are better than existing whole life plans, which are endowment products. These products cover individuals for 99 years and help to leave a corpus for the next generation. “While the returns may be low from these – at around 6 per cent – they can help to accumulate a corpus at low risk,” says Majumder.

Avoid real estate: Keep your legacy portfolio restricted to financial assets. Real estate has its challenges. “What if the beneficiaries are out of the country? Managing the properties sitting abroad will be difficult. Real estate is also difficult to liquidate,” says Sadagopan. Investment advisors say that most individuals own a house or two, which the next generation will anyway inherit after the owner passes away, so adding more real estate is not required. But if Real Estate Investment Trusts see the light of day, they can be a good investment option.

"Here are few meaningful ways to leave a bigger legacy for your heirs")