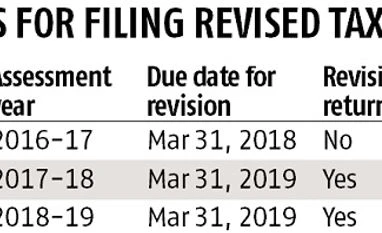

As can be seen, for FY 2015-16, the taxpayer can file a revised return by March 31, 2018. For FY 2016-17 and FY 2017-18, he will have to file by March 31, 2019. Revision of belated return is not permissible for FY 2015-16, whereas the same can be done from FY 2016-17 onwards.

To illustrate, ‘A’ filed his original tax return for the FY 2015–16 on July 20, 2016, ie, within the due date (July 31, 2016). Later on, while going through his banking records he realised that he had inadvertently missed reporting interest income from a fixed deposit. In this scenario, since his tax return was filed within the due date, ‘A’ has the option to rectify the aforesaid error by filing a revised tax return on or before March 31, 2018. If he hadn’t filed his original return within the due date, he would have lost the right to revise his return.

For FY 2016-2017, if ‘A’ files his original tax return on August 10, 2017, which is after the due date (July 31, 2017), he will still be entitled to revise his tax return on or before March 31, 2019, since the law has been amended to allow revision of a belated return for that year. Therefore, from FY 2016–17 even if the tax return is filed after the designated due date, one has the option to revise his tax return as per the earlier mentioned timelines for the respective financial year.

Challenges for expatriate employees With the change in the timeline for revision of tax returns, expatriate employees will face several challenges while claiming tax credit for taxes paid in overseas country. One, the reduction in time limit for revising the tax return may deny the benefit of such relief, especially where overseas tax returns are not filed or are not available by the end of the time lines as discussed in the above table. Two, filing of Form 67 will also be a challenge in the absence of documentation substantiating the claim of such relief.

These challenges are elaborated with an example. ‘A’, an Indian citizen, goes on an assignment to the US on December 1, 2017 and his residential status for FY 2017–2018 in India is Resident and Ordinarily Resident. Hence his global income is chargeable to tax in India for the aforesaid financial year.

He files his original return on the basis of his income information available before the due date, which is July 31, 2018. The return can be revised up to March 31, 2019. In order to offer his actual US income and claim the credit of the US taxes on the same in his India tax return, he requires his US return for the year 2017 and 2018.

Since the US follows the calendar year and has a due date of April 15 for filing the return, which can also be extended, it is unlikely that his US return for the year 2018 would be available before March 31, 2019. Therefore, A will be unable to claim the accurate or complete credit of foreign taxes for the year 2018 by the due date of March 31, 2019. Given the above challenge, one will have to wait and watch if the government provides any relief for this class of individuals.

While it is always better to be cautious and have all information available so that accurate details are reported while filing tax returns, one can still avail the opportunity provided by law to rectify mistakes in the tax return.

The writer is partner, Deloitte Haskins and Sells. The company’s Manager Bhavin Rajput and Deputy Manager Monish Satra contributed to the article

"Made an error? File your revised tax returns within stipulated timeline")