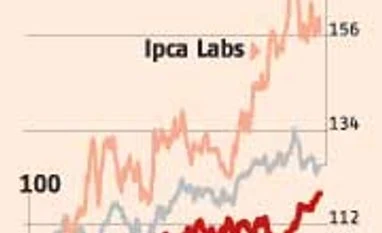

After a slew of upgrades by multiple brokerages, IPCA Laboratories could see a further re-rating, due to various growth drivers. The stock, which has seen a 27 per cent rise in six months and has already seen some P/E (price to earnings) re-rating over the past year, has more legs to run, say analysts.

Saniel Chandrawat and Sameer Baisiwala of Morgan Stanley expect the company to deliver a 23 per cent annual growth in earning per share over FY14-16, on the back of its steadily growing India formulations, further ramp-up in anti-malarials and easing of capacity constraints.

The key trigger continues to be US growth. This had been hampered over the past couple of years, due to capacity constraints. These meant no new products or increase in market share. With the company’s facility at the Indore Special Economic Zone expected to commence supplies from the June quarter of this year, the issue is likely to be tackled.

Credit Suisse analysts expect IPCA to re-rate further on improving cash flows and margin growth. While increasing scale is expected to add to cash flows, the proportion of the low margin and low growth Active Pharmaceutical Ingredient (API) business is expected to come down from 25 per cent now to 22 per cent in FY16. With the better earnings, analysts believe the company can sustain its FY15 P/E multiple of 16 times, which is a 20-25 per cent discount to large-caps and among the better bets among mid-cap stocks.

With target prices upwards of Rs 1,000, analysts expect returns of 20 per cent over the next year from this counter. Of the 38 analysts who track the stock, as many as 33 have a ‘Buy’ rating; five have a ‘Hold’, with no sell calls.

US a key trigger India sales are expected to grow faster than the domestic market at 15 per cent; the anti-malarial tender business should grow similarly. Even so, it is the US business which will drive overall sales, with growth estimated at a little over 40 per cent over the next couple of years. Though the company has approval for 18 products from the 38 Abbreviated New Drug Applications (ANDAs) filed so far, it has commercialised only seven.

In the recent past, the company filed products with low competition, such as Toprol XL (blood pressure), mesalamine (anti-inflammatory) and fenofibrate (cholesterol control), which should see higher sales. Joint managing director A K Jain says they’ll be launching the approved products over the next three or four months.

The high growth phase in the US over the next two years is also because product approvals have been bunched. IPCA was capacity-constrained due to the delay in approval of the Indore SEZ, say analysts at Credit Suisse. Revenues from the US, at $40 million, are expected to double by FY16 and the share of revenues from here are expected to improve from 7.5 per cent to 10 per cent, say analysts at Morgan Stanley. The company had entered the US market only in 2009; it now operates in this market through five partners, Ranbaxy being the largest. As of now, it has no plan for a front-end presence there.

India, Africa These two regions put together account for nearly half of IPCA’s overall revenue. The biggest chunk is its Indian formulations business. A majority of the revenue here comes from cardio vascular/diabetes (26 per cent), pain management (32 per cent) and anti-malarial drugs (15 per cent). Over the past five years, the company has been able to grow its India formulations business faster than the overall market, expanding revenue at a 15 per cent annual rate.

Going ahead, the company believes it will be able to grow its India business at 15-18 per cent yearly, against the sectoral growth rate of around 12 per cent. IPCA says the focus will be on improving the market share in existing products; a more measured approach will be taken on product launches.

The anti-malarial tender business, which supplies drugs to the African continent, is another major revenue earner. At Rs 400 crore, the Africa business accounts for 14 per cent of yearly income. The company is expected to grow this on the back of market share gains in existing products and increased sale of new products (such as artesunate injection, an anti-malarial) which are expected to be filed in the current financial year.

Sales in the rest of the world (Asian countries, Europe, CIS) are also expected to do well, growing 15-17 per cent annually over the next three years, estimate analysts. The only slow moving segment is API. This low-margin business is expected to grow in single digits (or in low double digits) in the medium term.

"US to be IPCA's new growth engine")