Market outlook 2018: Morgan Stanley more bullish on China than India

The research house has cut India's size in the portfolio by 100 basis points to accommodate Brazil's overweight stance where it expects a healthy economic growth

"Market outlook 2018: Morgan Stanley more bullish on China than India")

premium

WebinarsNew

Deep DiveNew

Explore Business Standard

The research house has cut India's size in the portfolio by 100 basis points to accommodate Brazil's overweight stance where it expects a healthy economic growth

"We reduce our overweight on India from +250 basis points (bps) to +150 bps previously. Key bull points for India in terms of the country model are increasing dividend yield trend relative to its country peers, combined with constructive views from our economist and country strategist. Weaker scores for India are its weak return on equity (ROE) and net margin trend," a Morgan Stanley report co-authored by Jonathan Garner, their chief Asia & emerging markets equity strategist says.

Also Read: Top 10 stocks Morgan Stanley recommends: Bajaj Finance, Maruti, ITC & more

However, they believe India is likely to remain in the midst of a domestic liquidity super cycle. Over the next 10 years, it expects $420 billion - $525 billion in domestic equity inflows that could have the power to keep India's relative multiples higher for longer. That said, the two key risks for India, according to the research house, are the rising oil prices and the fact that 2018 will see a number of state / assembly elections, which can keep the markets volatile.

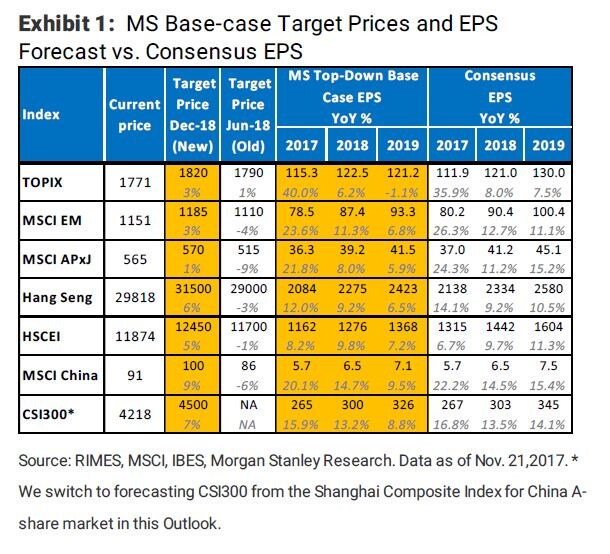

CLICK HERE FOR GRAPHIC ON COUNTRY-WISE TARGET PRICES

Going ahead, Morgan Stanley expects 2018 to be a tough year for the markets even though there are catalysts supportive of a continued rally. Central bank tightening globally and balance-sheet reduction in the US, slowdown in growth in China, busy election calendar in the Asia pacific region (ex-Japan) and a rise in oil prices are some of the key things that the markets will have to grapple with.

Also Read: Sensex at 100,000, m-cap at $6.1 tn: 7 takeaways from Morgan Stanley report

In the Indian context, the research house expects the real gross domestic product (GDP) growth to accelerate to 7.5% in FY19 and to 7.7% in FY20, from 6.7% in FY2018, as the economy has already worked off the headwinds posed by demonetisation and the implementation of the goods and services tax (GST) bill. A pick-up in growth and consumption, in turn, will help boost private capex.

In terms of sectors, they still continue to prefer banks; remain overweight on capital goods, food & beverage and tobacco sectors. Pharmaceuticals, household and personal products (FMCG) remain their key underweights in the Indian context.

"For India Household & Personal Products, stocks look rich and margins are likely to decline due to higher material costs and competition, and are therefore a headwind to the earnings outlook. We also remain underweight on the largest pharma name - Sun Pharma - where we believe earnings should compress in the near term in view of lower US business - lack of new approvals, delay in Halol resolution, pricing risk at Taro portfolio - and higher opex (specialty front-end/R&D)," the report says.

Already subscribed? Log in

Subscribe to read the full story →

3 Months

₹300/Month

1 Year

₹225/Month

2 Years

₹162/Month

Renews automatically, cancel anytime

Premium stories handpicked daily by our editors

News, Games, Cooking, Audio, Wirecutter & The Athletic

Digital replica of our daily newspaper — with options to read, save, and share

Insights on markets, finance, politics, tech, and more delivered to your inbox

In-depth market analysis & insights with access to The Smart Investor

Repository of articles and publications dating back to 1997

Uninterrupted reading experience with no advertisements

Access Business Standard across devices — mobile, tablet, or PC, via web or app

First Published: Nov 27 2017 | 11:36 PM IST

{kind=link}