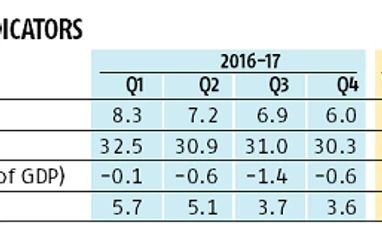

The recent (IMF) report on the Indian economy projects a gradual acceleration of growth but also draws attention to several downside risks. The report uses circumspect language about demonetisation and the botched implementation of the goods and services tax (GST) but is quite explicit on the growth impact. In medical language, the Indian economy is recovering from some recent traumas but is still convalescing and runs some risks of relapse.

The GST could have been implemented more intelligently, with the phased introduction of net-based reporting and a simpler tax structure. But the basic gains of a single tax structure in the country and a cooperative federal system for managing the GST are significant achievements with substantial long-term benefits, particularly if the rationalisation and simplification recommended by many are implemented. There was a price, which could have been less had the implementation been better prepared. But the long-term gain is substantial. However, in the case of demonetisation, one can hardly argue that the purported gains in digitisation of payments (increasingly under question) and tax compliance justify the drastic measure. Demonetisation was a badly conceived and a badly implemented measure that cost the economy dear.

Fiscal prudence in the form of deficit containment can play a positive role in boosting growth because it would reduce the government’s draft on private financial savings which at the moment is nearly 70 per cent. Today the government cannot afford to let go its control over about 70 per cent of banking and insurance assets as it relies on that for resources through requirements such as the statutory liquidity ratio (SLR) in banks and investment directions that serve its interests rather than those of depositors or policyholders. They are doing precisely what nationalisation was supposed to correct — the diversion of resources by owners for their own needs rather than maximising returns for depositors and policyholders. The IMF report recognises this elephant in the room but has little to add beyond the usual exhortations about better governance.

Denationalisation of public sector financial institutions is not the answer — not just for political reasons, but also because we do not have a private sector that can operate financial institutions independently of linked corporate interests. The few successful private banks that we have are independent because they are largely owned by foreign institutional investors.

Distancing public sector banks and insurance companies from direct governmental control will lead to a healthier capital market. It can reduce future non-performing asset risks, enlarge and strengthen the debt market and ensure depoliticised oversight over corporate management by major domestic institutional investors such as Life Insurance Corporation. This is essential for accelerating growth in the medium term and making other areas of structural change more acceptable and easier to implement. If we can liberate monetary policy from political control, why can we not do the same for supervision of public sector financial institutions?

"The state of the economy")