The Indian automotive fuel market is hotting up with the Union government granting permission to seven entities to retail liquid and alternative fuel. Among those is Reliance Industries Ltd (RIL) that needed the government re-approval because of a business restructuring. With this, there will be some 14 players in the domestic petroleum industry’s marketing business. Despite this, the government’s role in the pricing of fuel continues to be unclear.

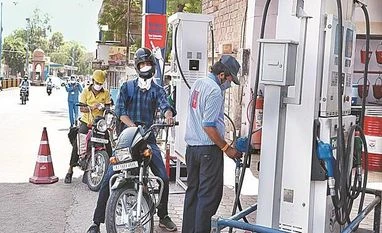

Officially, the Union government maintains an arm’s-length relationship in the retail pricing of petrol, diesel and even compressed natural gas (CNG). Yet, it continues to have a say in what consumers pay, both in the form of taxation tweaks as well as through informal directives to state-owned oil marketing companies (OMCs).

The OMCs, for instance, did not change retail prices for the period covering the monsoon session of Parliament because of the strong criticism against the government for high diesel and LPG prices. Nor has the government reduced levies that constitute 32 per cent of petrol and 35 per cent of diesel prices in Delhi even though fuel prices are at record highs.

Union Finance Minister Nirmala Sitharaman has now cited fiscal constraints for not reducing fuel taxes even though global benchmark prices have risen, hurting the consumer pocket. She cited as a reason the repayment burden on oil bonds issued under the predecessor United Progressive Alliance (UPA) to OMCs.

Oil bonds worth Rs 1.34 trillion were issued during 2005-2010 to subsidise retail prices without any cash outgo from the government. The annual outgo on account of these bonds, however, is around Rs 10,000 crore whereas the Centre collects over Rs 2.8 trillion as its share of tax on petroleum products.

There is, meanwhile, no official reason for prices not changing, though OMCs shifted to daily price change for petrol and diesel in 2017. It is believed that the companies were holding prices for political exigencies of a Parliament session and preparation for state Assembly elections.

This is ironic because the National Democratic Alliance (NDA) government introduced complete diesel price deregulation in October 2014, after it decided to end the UPA policy for phased decontrol. This was nearly four years after the UPA decontrolled petrol price in 2010.

The Atal Bihari Vajpayee government had, in fact, dismantled the administered price mechanism (APM) in 2002 after which RIL, Essar Oil and Shell entered the fuel retailing business. By 2004, these private players started making a dent in the OMCs’ market share but the competition soon collapsed because the government never really gave up pricing control.

The subsidy available only to OMCs ensured that private players could not compete with them. Essar and Shell, however, somehow continued with their retailing business though RIL mothballed some of its outlets.

When petrol and diesel prices were finally decontrolled, the private players made a second attempt at fuel retailing. Prices are, however, still not free because they are calculated on a 15-day rolling average of global benchmarks, implying that OMCs follow a formula-based pricing. The setting of retail prices, the frequency with which they change and the government increasing taxes when global prices are low all put a question mark on the so-called market-linked pricing mechanism.

With the new authorisations, the competitive challenge, however, will not just come from the sheer number of players, but also the range of fuel options that is now available to consumers. The choice of automotive fuel, in fact, is much wider than what it was almost two decades ago when the APM was dismantled.

The recent authorisations of seven retailers, barring the one given to Reliance BP Mobility Ltd (RBML), has players that have little experience in fuel retailing. This is in contrast to 2002, primarily because the permission regime for retailing has been relaxed.

“An entity seeking authorisation for retail marketing only should have a minimum net worth of at least Rs 250 crore at the time of making the application to the Central Government for grant of authorisation. Accordingly, it would be required to submit the audited accounts statement of the previous financial year in support of its application,” said a November 2019 notification. The entity would also be required to ensure that its net worth does not fall below Rs 250 crore at any point during the tenure of the authorisation.

The first set of permissions after dismantling of APM was, however, granted only to those who could make an investment of Rs 2,000 crore in the petroleum sector or by extending a similar guarantee.

The operational requirements are, nonetheless, stricter this time with a minimum of at least 100 retail outlets being set up, out of which at least five per cent should come up in notified remote areas within five years of the authorisation being granted. So it will soon be the likes of Onsite Energy and MK Agrotech posing a challenge to Indian Oil Corporation, the market leader, Hindustan Petroleum Corporation, Bharat Petroleum Corporation (of which Vedanta is one of the suitors), RIL-BP, Rosneft-backed Nayara Energy and Shell.

A David versus Goliath game, where the incumbents are big companies while the new players are much smaller with no refineries of their own, will now play out.

"Fuel paradox: 6 more pvt players on cards, but price reins still with govt")