Bonds to rally after small savings rate cut

Reserve Bank could cut policy rates by 50 bps instead of 25

Anup Roy Mumbai While savers are crying hoarse over the government reducing the interest rates on small savings schemes, the move has been welcomed by the bond market. Bond yields are set to fall on hope that the Reserve Bank of India (RBI) would now cut its policy rate by 50 basis points (bps), instead of the expected 25.

One basis point is a hundredth of a percentage point. As yields fall, prices of bonds rise. The RBI is scheduled to review its monetary policy on

April 5. After the Budget, in which the government managed to keep its fiscal deficit within the targeted 3.5 per cent of gross domestic product, bond yields have already fallen 25 bps, adjusting for an equal quantum of rate cut by the central bank in the April policy.

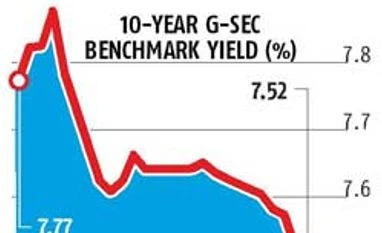

The 10-year bond yield closed at 7.52 per cent on February 18, down from 7.8 per cent before the Budget, despite the banking sector liquidity drying up drastically in recent times.

Banks had to borrow an unprecedented Rs 2.7 lakh crore from the RBI recently as advance tax outflow drained lenders' liquidity. The surplus cash balance of the government meant for auction is now Rs 1.92 lakh crore. While the central bank does not disclose the actual balance, economists estimate the auction part to be 70-80 per cent of the actual cash.

Banks have maintained that high small savings rate prevents them from lowering their deposit rates and thus the lending rate. They will now have to toe the line and cut their deposit rates aggressively.

According to a PTI story, bankers would still wait for the policy cues from the RBI. However, they are not averse to rate cuts. A combination of deposit rate cut and softening bond yields will force banks to lower their lending rates under the marginal cost-based lending rate (MCLR) regime that will kick in from April 1.

That's positive for bond yields.

"Bond yields will definitely fall by at least five bps on Monday," said Devendra Dash, a senior bond trader with DCB Bank. "By the RBI policy date, bond yields can fall by 10-15 bps if there is no adverse development."

The tight liquidity situation should improve from the start of the financial year as the government is expected to start spending its surplus cash balances with the RBI soon after the new financial year starts April 1. This should allow banks to invest in government bonds more and drive down yields further.

"The liquidity situation is the biggest driving force now. Bond yields can fall further, but a lot of discounting has already happened and a further fall will be determined by available liquidity," said Harihar Krishnamurthy, head of treasury at First Rand Bank, adding a steeper rate cut by the RBI in these situations might not aid much.

"Right now, the market does not need a 50 bps; a 25 bps will do," said Krishnamurthy.

"Bonds to rally after small savings rate cut")