Backed by attractive valuation, expected pick-up in credit growth, decline in credit costs, and stronger balance sheets, Indian bank and non-bank finance companies (NBFCs) may reverse their underperformance in the new calendar year 2022, say analysts.

So far in 2021, the Nifty Bank index has rallied 18.6 per cent on the National Stock Exchange as against a 25.2 per cent gain in the benchmark Nifty50 index, data show. The Nifty Financial Services index, meanwhile, is up 19.4 per cent YTD. However, during the past one month, the Nifty Bank declined 4.9 per cent on the NSE relative to the Nifty's 2.8 per cent fall. The Nifty Financial Services index, too, slipped 4.4 per cent.

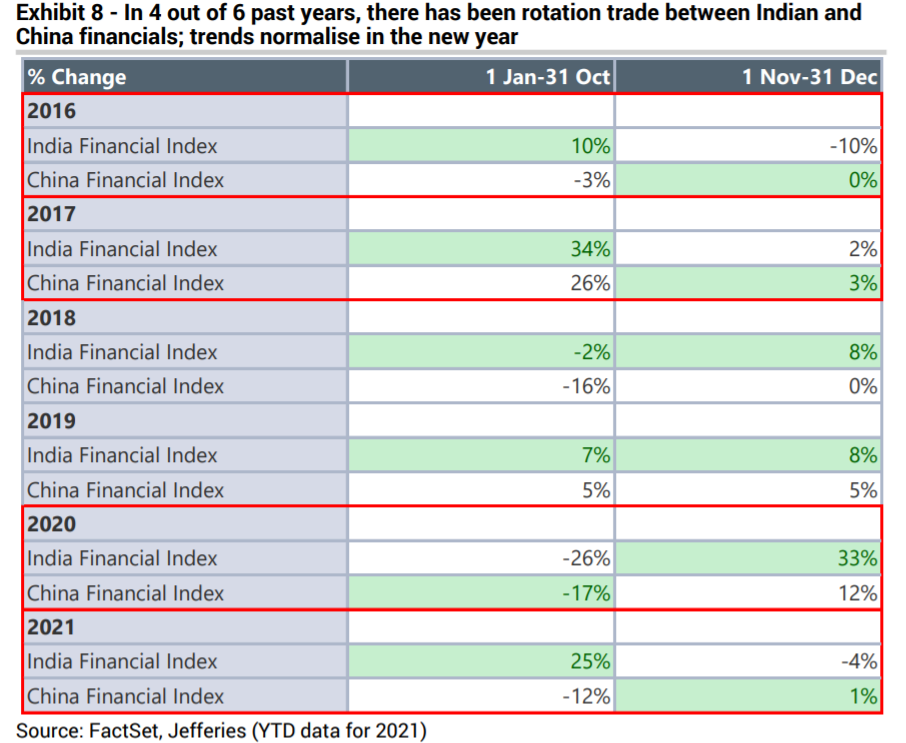

"On the back of Indian financials' YTD outperformance, there has been rotation trade away from India as was evident in 4 out of 6 years. Rotation trades normalise into the New Year and Indian bank's growth pick-up and valuations can support it," said Prakhar Sharma, equity analyst at the brokerage, in a co-authored note with Abhishek Khanna and Bhaskar Basu.

Secondly, a pick-up in credit growth and decline in credit costs may lead to doubling of profit over FY21-24, believe analysts at Jefferies.

"With corporate balance sheets mended, PLI-schemes supporting investments, and lending to small and medium enterprises (SME) improving, the bank credit is expected to grow 10 per cent over the next 12 months and further thereafter. Given this, over FY21-24, we see this driving a 17 per cent CAGR in core operating profits for private banks and 8 per cent for public sector banks," the brokerage noted.

With low restructuring and quality of ECLGS-loans (emergency credit line guarantee scheme) holding-up, analysts at Jefferies see credit costs to drop from 2.2 per cent of average loans in FY21 to 1.5 per cent in FY23/FY24. This, they believe, will support near doubling of earnings for the sector over FY21-24 with upside if banks dig-into their buffer provisions.

Analysts at CLSA, too, believe normalised asset quality and rising interest rates could lead to upside in net interest margins (NIMs) in the near-term.

As regards NBFCs, Subramanian Iyer, equity analyst at Morgan Stanley, opine they are carrying excess liquidity on their balance sheets and ALM (asset-liability management) is very conservative, which augur well for the sector.

"Improving economic activity, and strengthened balance sheet buffers will help assets under management (AUM) of NBFCs to grow 8-10 per cent next fiscal," highlights a report by Crisil Ratings Agency. That compares with an estimated growth of 6-8 per cent this fiscal and 2 per cent last fiscal.

Given the above tailwinds, Morgan Stanley is overweight on Bajaj Finance, Cholamandalam Investment and Finance, Shriram Transport Finance, and HDFC. Those at Jefferies are bullish on HDFC Bank, ICICI Bank, SBI, and HDFC.

"We see favourable risk/reward for banks with ICICI Bank as top pick and now include HDFC Bank among top calls given growth rebound and fair valuations," the brokerage said.

"Banks, NBFCs set to reverse underperformance in 2022, say analysts")

{kind=link}