RBI Governor Das, bankers may not be on same page over passing rate cuts

So far, SBI has reduced its home loan rates (up to Rs 30 lakh) by only five basis points (bps) after the policy rate cut of 25 bps on February 7

"graph")

premium

graph

Reserve Bank of India (RBI) Governor Shaktikanta Das will meet bank chiefs on Thursday to impress upon the need to improve transmission within the confines of it being a business decision. However, certain indicators suggest that bankers won’t be wrong in disagreeing with Das on the all-important rates issue.

So far, only State Bank of India (SBI) has reduced its home loan rates (up to Rs 30 lakh) by only five basis points (bps) after the policy rate cut of 25 bps on February 7.

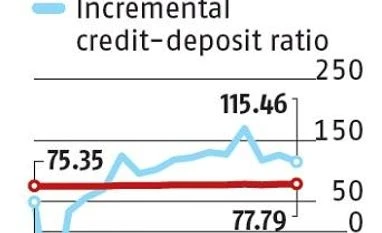

High credit deposit (CD) ratio, with incremental ratio over 100 (indicating credit disbursement is more than deposit mobilisation) leaves banks with no room to cut deposit rate. They cannot cut lending rates without cutting deposit rates. Even when deposit rates are pared, because of their fixed nature, the cost of deposit doesn’t come down readily. Contrary to that, the lending rate cut immediately translates into hit on profitability.

Pallab Mahapatra, managing director and chief executive officer of Central Bank of India, said his bank’s marginal cost-based lending rate (MCLR) for one year and deposit rates are already lower than many large banks. For reducing loan rates further, the bank will have to cut deposit rates further, which would make the bank vulnerable to poaching for deposits from competing banks. And this, therefore, makes transmission a challenge.

So far, only State Bank of India (SBI) has reduced its home loan rates (up to Rs 30 lakh) by only five basis points (bps) after the policy rate cut of 25 bps on February 7.

High credit deposit (CD) ratio, with incremental ratio over 100 (indicating credit disbursement is more than deposit mobilisation) leaves banks with no room to cut deposit rate. They cannot cut lending rates without cutting deposit rates. Even when deposit rates are pared, because of their fixed nature, the cost of deposit doesn’t come down readily. Contrary to that, the lending rate cut immediately translates into hit on profitability.

Pallab Mahapatra, managing director and chief executive officer of Central Bank of India, said his bank’s marginal cost-based lending rate (MCLR) for one year and deposit rates are already lower than many large banks. For reducing loan rates further, the bank will have to cut deposit rates further, which would make the bank vulnerable to poaching for deposits from competing banks. And this, therefore, makes transmission a challenge.