Flip-flop on taxing indirect transfers

Tax experts expect significant clarifications in the Budget to address double-taxation concerns

"data")

premium

data

On December 21, the Central Board of Direct Taxes (CBDT) issued a circular clarifying that offshore vehicles, including foreign portfolio investors (FPIs), were subject to indirect transfer provisions. The move set alarm bells ringing in fund houses from Hong Kong to London and New York.

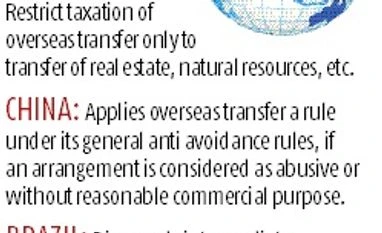

Effectively, the indirect transfer provisions imposes taxes on offshore transactions if the value of Indian assets represent 50 per cent or more of the value of all assets owned by the FPIs.

The circular contained responses to queries on the indirect transfer provisions in a number of different contexts, such as redemptions by offshore funds registered as FPIs, master-feeder structures, and corporate reorganisations. “While the expectation was that the circular would examine the practical problems being faced by stakeholders and propose rectifications to the indirect transfer provisions or, at least, relax the rigours arising from a mechanical application of the existing provisions, the circular instead confined itself to an excessively literal interpretation and provided little guidance to stakeholders,” a note by Mumbai-based law firm Nishith Desai Associates said.

Following representations from individual funds, including FPIs, venture capital funds and industry bodies such as the Asia Security Industries & Financial Markets Association (Asifma), the government decided to keep the operation of this circular in abeyance. While the move has come as a temporary relief, foreign investors still see the sword of double-taxation hanging above their hard-earned returns. They expect the upcoming Budget to take significant steps to address the issue in a wholesome manner.

Tax more than gains

Some officials say the funds and consultants brought it upon themselves by bombarding the government with queries on how the law would apply in different situations. On June 15, the CBDT had constituted a working group to examine the issues raised by stakeholders with respect to the indirect transfer provisions added in the Indian tax rules in 2012. After considering the comments of the working group, the CBDT, through the December circular, issued clarifications on the concerns raised in the format of answers to frequently asked questions. As many as 19 situations were addressed in the circular.

Effectively, the indirect transfer provisions imposes taxes on offshore transactions if the value of Indian assets represent 50 per cent or more of the value of all assets owned by the FPIs.

The circular contained responses to queries on the indirect transfer provisions in a number of different contexts, such as redemptions by offshore funds registered as FPIs, master-feeder structures, and corporate reorganisations. “While the expectation was that the circular would examine the practical problems being faced by stakeholders and propose rectifications to the indirect transfer provisions or, at least, relax the rigours arising from a mechanical application of the existing provisions, the circular instead confined itself to an excessively literal interpretation and provided little guidance to stakeholders,” a note by Mumbai-based law firm Nishith Desai Associates said.

Following representations from individual funds, including FPIs, venture capital funds and industry bodies such as the Asia Security Industries & Financial Markets Association (Asifma), the government decided to keep the operation of this circular in abeyance. While the move has come as a temporary relief, foreign investors still see the sword of double-taxation hanging above their hard-earned returns. They expect the upcoming Budget to take significant steps to address the issue in a wholesome manner.

Tax more than gains

Some officials say the funds and consultants brought it upon themselves by bombarding the government with queries on how the law would apply in different situations. On June 15, the CBDT had constituted a working group to examine the issues raised by stakeholders with respect to the indirect transfer provisions added in the Indian tax rules in 2012. After considering the comments of the working group, the CBDT, through the December circular, issued clarifications on the concerns raised in the format of answers to frequently asked questions. As many as 19 situations were addressed in the circular.