There are legitimate questions that might be asked whether the fiscal deficit has indeed been contained and will be contained to the headline levels. The FM has been far more transparent than has been the practice in recent years, by making some extra-Budgetary borrowing explicit, and showing how much that pushes up the actual fiscal deficit. However, the fact remains that some other borrowing by quasi-government agencies is not reflected here.

That said, however, it seems much clearer than before what the government’s fiscal situation is. Which is one reason why, possibly, the bond markets might take a very different view of the Budget from the equity markets. Market borrowing for the government in the coming year is, according to the Budget Estimates, lower than expected. The question is if the bond markets will be able to respond. Expectations that foreign investors, for example, would lap up Indian bonds have not exactly been the case in practice. As of right now, according to the Clearing Corporation of India, of the limit of Rs 2.46 trillion for the “general” category of foreign portfolio investors in Indian government securities, only Rs 1.74 trillion — just over 70 per cent — is utilised. The Reserve Bank of India has attempted to address this last month by raising the ratio of their total investment that FPIs can put into short-term securities. However, HSBC analysts have noted that “the demand dynamics for INR bonds are unlikely to change in the near term” as a consequence of the Budget, “especially with India government securities recording net selling by foreign investors in recent months”.

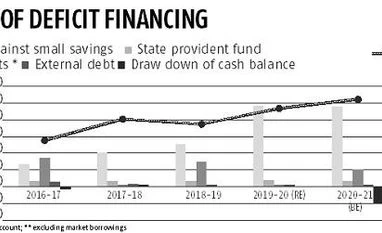

The big bonanza, however, will be if Indian bonds are included in global bond indices. In effect, this would enable funds from larger passive investors to finance Indian government deficits. The idea is that this would both ease the strain on Indian domestic resources and also avoid the dangers of dependence on short-term flows for financing government deficits. Certainly, it would be a better way of financing the deficit than depending upon the National Small Savings Fund (NSSF), which appears to be the current approach. The NSSF is being treated as a piggy bank for spending, which is clearly unsustainable.

The Budget includes some announcements that seem to be related to this effort. Ms Sitharaman’s speech included the promise that “certain specified categories of Government securities would be opened fully for non-resident investors”, though it is not yet clear what this means in practice. A related question is whether corporate bonds will also benefit; Principal Economic Advisor Sanjeev Sanyal talked about how new legislation promised for bilateral netting might help develop credit-default swaps and thus deepen the corporate bond market.

On some level, the effects on the bond and equity markets should be seen together. What is happening is that the Indian government is now stuck living beyond its means. It is not paying its bills to such entities as oil-marketing companies, fertiliser companies and the like; it is delaying payments to states; it is not following through on Budgeted discretionary and capital expenditure. As a rule of thumb, about two-thirds of the expenditure of the Union government is “tied” — it is difficult to reduce. Thus the burden of reduced revenue falls upon the remaining third of expenditure, which has been squeezed — but also upon the financial markets generally. Given that there is significant resistance to issuing dollar-denominated debt, as was made clear last year, we are left with a dependence upon domestic financial markets. The capability of the latter to finance the deficit depends upon their size, which depends in turn upon the size of financial savings of households and of foreign inflows. Higher disinvestment receipts mean that there is less financial household savings — which constitute perhaps 10 per cent of GDP — for other equity market participants to mop up. More government paper in the bond markets has traditionally had a similar crowding-out effect. Foreign participation in the equity markets is, by many people’s thinking, incentivised as much as it can be. The only path therefore left to expand the pool of finance that can prop up deficits is by increasing foreign participation in the debt market. Essentially, the government has few other options remaining. The immediate impact of the crisis is thus being felt in the government’s increased openness to foreigners financing its deficit.

There are two crucial questions left. First, if such inflows materialise, what will be the effect on the rupee’s value — and therefore on exports growth, the only sustainable path to recovery? And second, will attempts to increase this flow of funds into India effectively focus on a channel to government spending over what should be the focus — a channel from global finance to domestic private-sector, long-term investment?

m.s.sharma@gmail.com , Twitter: @mihirssharma  "Crowding out and opening up")