Three NBFCs to bet on as CV sales recover

Piggybacking on visible recovery in sales of commercial vehicles, Shriram Transport Finance, M&M Financial and Cholamandalam Finance emerge favourites

"Three NBFCs to bet on as CV sales recover")

With many quarters of earnings disappointment on account of weak net interest income (NII) growth or elevated non-performing assets (NPAs), stocks such as Shriram Transport, M&M Finance and Cholamandalam Finance have remained under pressure. Now, with the monsoon likely to be better than average and sales of commercial vehicles (CVs) showing steadfast signs of improvement, these stocks gained between 14 and 30 per cent in the past month. Their March quarter (Q4) results, exceeding the Street’s expectations, has also fuelled their stock performance, regenerating interest in these.

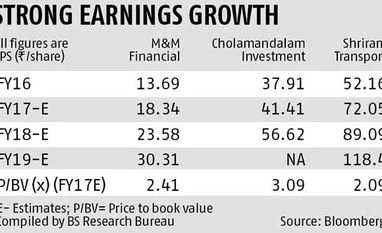

For instance, Shriram Transport, market leader in the CV lending segment, saw its NII for Q4 expand to Rs 1,273 crore, up 34 per cent over a year. However higher provisioning (Rs 1,073 crore, up 33 per cent) dented net profit to Rs 143 crore, down 55 per cent. However, as this was due to consolidation of its commercial equipment business, analysts regard it as a one-off. In fact, the 23 per cent year's growth in assets under management or AUM (Rs 72,750 crore), and positive surprise from the share of new CVs expanding from eight per cent a year before to 10 per cent, offset the decline in profit. Used vehicles, the rest of its business, grew 21 per cent over a year. AUMs in FY17 are expected to grow by 15 per cent, contingent on the monsoon.

As a result, analysts at Jefferies have raised their earnings per share (EPS) target for FY17-18 by 100–200 basis points (bps), as Shriram Transport should benefit from strong CV credit demand and lower borrowing cost.

Likewise for M&M Financial Services. After a watered-down December ‘15 quarter, NII and net profit posted 16 per cent and 12 per cent growth over a year in Q4. Elevated provisioning for bad loans, major pain point for many quarters, showed remarkable improvement, down 23 per cent year-on-year to Rs 116 crore. Also, with fairly high levels of repossession and collection efforts in place, analysts at Credit Suisse note the provision coverage for M&M Financial remains intact at 62 per cent. Though loans grew 11 per cent over a year (versus 18-20 per cent for peers), Credit Suisse has, with the asset quality improving, recently upgraded its EPS target for FY17 by 300 bps to Rs 23.6.

For instance, Shriram Transport, market leader in the CV lending segment, saw its NII for Q4 expand to Rs 1,273 crore, up 34 per cent over a year. However higher provisioning (Rs 1,073 crore, up 33 per cent) dented net profit to Rs 143 crore, down 55 per cent. However, as this was due to consolidation of its commercial equipment business, analysts regard it as a one-off. In fact, the 23 per cent year's growth in assets under management or AUM (Rs 72,750 crore), and positive surprise from the share of new CVs expanding from eight per cent a year before to 10 per cent, offset the decline in profit. Used vehicles, the rest of its business, grew 21 per cent over a year. AUMs in FY17 are expected to grow by 15 per cent, contingent on the monsoon.

As a result, analysts at Jefferies have raised their earnings per share (EPS) target for FY17-18 by 100–200 basis points (bps), as Shriram Transport should benefit from strong CV credit demand and lower borrowing cost.

Likewise for M&M Financial Services. After a watered-down December ‘15 quarter, NII and net profit posted 16 per cent and 12 per cent growth over a year in Q4. Elevated provisioning for bad loans, major pain point for many quarters, showed remarkable improvement, down 23 per cent year-on-year to Rs 116 crore. Also, with fairly high levels of repossession and collection efforts in place, analysts at Credit Suisse note the provision coverage for M&M Financial remains intact at 62 per cent. Though loans grew 11 per cent over a year (versus 18-20 per cent for peers), Credit Suisse has, with the asset quality improving, recently upgraded its EPS target for FY17 by 300 bps to Rs 23.6.

In the case of Cholamandalam Finance, Phillips Capital has increased its EPS estimate for FY17 by 350 bps to Rs 48, on the back of strong NII, net profit and disbursements in the March quarter. While NII at Rs 600 crore grew 33 per cent over a year, net profit expanded 42 per cent to Rs 192 crore. Vehicle finance (mainly CVs) accounts for 67 per cent of Cholamandalam’s assets. In FY17, the company expects to maintain 20 per cent growth in advances, with higher focus on heavy CVs.

A word of caution, though. While the asset quality might improve in FY17, with an above-average monsoon, the crunching of provisioning norms from 120 and 150 days per dues to 90 dpd by FY17 (or FY18 in the case of Shriram Transport) could put some stress on asset quality. But, as this is a structural change, the Street is not too wary.

Don't miss the most important news and views of the day. Get them on our Telegram channel

First Published: May 09 2016 | 10:46 PM IST