RBI's pause on rate cuts brings credit opportunity funds under spotlight

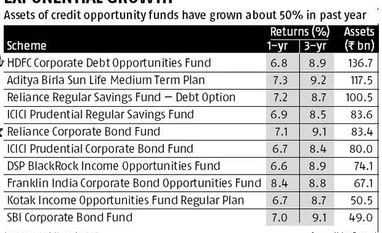

Assets of these funds are up 50% in 2017 at Rs 1.1 trillion

"graph")

premium

Last Updated : Jan 01 2018 | 11:29 PM IST

With interest rates likely to rise or remain on hold in the near future, debt funds that look beyond AAA-rated paper for higher yields are back in the limelight. These include credit opportunity and corporate bond opportunity funds.

In the previous 11 months, assets of these funds have grown nearly 50 per cent to Rs 1.1 trillion from Rs 745 billion, data from Value Research shows. In the past year, these funds have given returns of 7.4 per cent. HDFC Corporate Debt Opportunities Fund is the largest fund in this category, with assets more than Rs 130 billion.

The pause in the rate-cut cycle has limited opportunities for funds that rely on duration play, as these funds primarily benefit in a declining interest rate environment. Bond prices and interest rates move inversely.

“It appears there has been some shift in money from the underperforming duration funds to credit opportunity funds by investors chasing returns,” said Vidya Bala, head of mutual fund research, FundsIndia.com.

Over the course of the past one year, the Reserve Bank of India (RBI) has become hawkish due to a rise in oil prices and the possibility of fiscal slippage. Yields of the 10-year government securities rose 81 basis points (bps) in 2017 to 7.326 per cent.

Interest rates were likely to remain on hold or rise, making longer duration products unattractive, said experts.

“While G-sec yields may remain elevated, the possibility of improved corporate profitability and increase in ratings upgrades makes credit opportunity funds relatively more attractive at this point,” said R Sivakumar, head-fixed income, Axis Mutual Fund.

Accrual funds such as credit opportunity or corporate bond opportunity funds do not play the interest rate game but seek to gain from higher accrual in corporate bonds that do not enjoy high credit ratings. They might also benefit from rating upgrades, which can lead to gains from price appreciation. While these funds might be less volatile than duration funds, they come with a higher risk of capital loss.

Portfolio’s ratings mix, diversification and liquidity are the three key risk factors that investors need to look at before investing in these funds. “Lower-rated papers carry elevated risks and investors need to assess the relative percentage of AAA-rated papers vis-a-vis the non-AAA ones,” said Sivakumar.

MFs do not look at papers that are below long-term A-rated. But they can technically go up to BBB, which is considered investment grade. Going below this requires permission from the fund’s trustees.

After the Amtek Auto episode in 2015, investors and funds are taking greater precaution while selecting papers. Apart from third-party credit ratings, several fund houses now relying on in-house research teams to assess the quality of papers they invest in.

“Credit opportunity funds are the equivalent of holding a sector fund in an equity portfolio. Not more than 20 per cent of a debt portfolio can be exposed to these funds, provided the holding period is three years or more,” said Bala. Further, investments in such funds should be combined with investments in higher-quality income accrual funds in the short to medium term, she added.