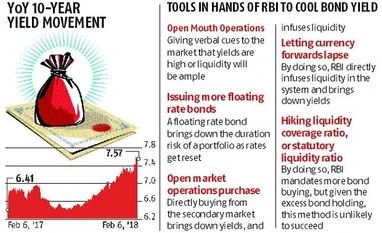

Here are the tools available to RBI to manage surge in bond yields

The central bank can openly buy from the secondary market through its open market operations programme

"RBI, bond yields")

..

With rapid rise in yields, a section of the market expects the central bank to send out guarded signals about its future strategy on yield management in its Wednesday monetary policy announcement.

In market argot, this is called ‘open mouth operations’ and typically involves the governor, or deputy governor, telling the market through the media that the yields have moved too much and need to ease. If needed, the central bank will pump in more liquidity or buy bonds to increase demand of fixed income papers, thereby bringing down yields.

Senior bond dealers and treasurers say there are many tools with the Reserve Bank of India (RBI) that can effectively address stress in the market. But these tools are used judiciously to preserve their efficacy.

Insofar as cost effectiveness goes, communication is the cheapest mode of market intervention. But there are elaborate tools that a central bank can undertake. But there will be varied costs involved in other modes as well.

Also Read

Though there is no leeway left in the current scenario, one effective way of cooling yields in a short period is by cancelling auctions. Since supply is curbed, yields nosedive at every announcement of cancellation. However, now there is only one auction left and that too could get cancelled; the government could make do with short-term treasury yields for this year, news agencies reported, quoting finance ministry officials. The 10-year bond yields corrected sharply to close at 7.568 per cent from their intraday high of 7.63 per cent on this news.

In case the central bank is not able to cancel bond auctions, one effective way of curbing yields is by introducing more floating rate bonds. Since floating rate bonds have a coupon reset every six months, the problem of mark-to-market doesn’t arise. Besides, the duration risk of bonds gets addressed. However, floating rate bonds are not issued easily as adverse yield movement would mean the government would have to pay a higher coupon each time.

The central bank has already adopted this approach, as can be seen by the auction plan for Friday. Of the Rs 110 billion scheduled Friday’s auction, Rs 80 billion will come from 10-year bonds, which have ready takers, the rest Rs 30 billion will come from a floating rate bond.

The central bank can openly buy from the secondary market through its open market operations programme. By doing so, the central bank pumps in liquidity and pushes up demand for bonds at the same time. It comes at a cost for the central bank. But as the country advances towards an election year, and currency slippages are guaranteed, the RBI may have to increase liquidity via bond purchases.

If everything else fails, the RBI can simply let the forwards lapse. The central bank has a formidable $30.6 billion net forward position. If the central bank decides to not roll over the whole, or even a part of it, the market could be flush with liquidity and the bonds yields would cool off sharply. However, by doing so, the rupee would come under pressure and that might have an implication for imports, and consequently on inflation. That’s why it is also the last resort for any central bank, say experts.

In the third quarter, banks collectively lost at least Rs 150 billion because the 10-year yields moved up 70 basis points (bps). So far in the fourth quarter, yields have moved up 23 bps. The quarter is two months to close, but if this trend continues, the banks will have reasons to panic.

However, the US 10-year treasury corrected from its near 2.9 per cent level to trade at the 2.7 per cent level. If the US yields cool off, Indian yields will not harden much either, say bond dealers. In that case, just the RBI’s ‘open mouth operations’ would suffice to keep yields in check.

More From This Section

Don't miss the most important news and views of the day. Get them on our Telegram channel

First Published: Feb 07 2018 | 5:55 AM IST