Bracing for macro-data, news flow

December is likely to see a rate hike from the Fed and Brexit-related fluctuations in the GBP

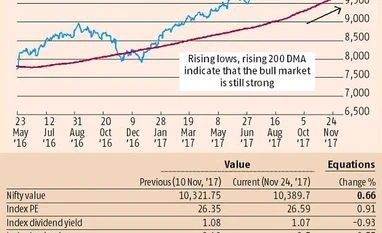

"Graph")

premium

This fortnight is likely to be driven by macro-data and news flow. The bulk of Second Quarter 2017-18 (Q2, July-September 2017) results are in. The GDP data is released this week. The Reserve Bank of India (RBI) has a policy review next week and PMI (Purchasing Managers’ Index) data will also come in.

Abroad, the US Federal Reserve has a policy review next week and a new Federal Reserve chairperson is also due to be confirmed. The OPEC meets this week to reach consensus on crude production in 2018. China stocks had a meltdown on Thursday. Angela Merkel’s government is struggling and there’s the possibility of a snap German election. The Brexit drama continues.

The markets must discount disagreement between S&P and Moody’s on sovereign ratings. There’s an important change, via ordinance, in the IBC (Insolvency and Bankruptcy Code). Beyond the economics, many traders will sit on the fence until the Gujarat and Himachal election results.

The Q2 results were lumpy in sector contributions and had a positive bias for larger firms. A study by Business Standard of 1,850 listed companies shows overall revenue grew 8.7 per cent year-on-year while net profits declined YoY by 2.6 per cent. The Nifty’s net profits were up by 12 per cent. Those 50 companies accounted for over 80 per cent of the combined net profits of the sample (up from 78 per cent YoY). There have been some cuts to consensus estimates.

Abroad, the US Federal Reserve has a policy review next week and a new Federal Reserve chairperson is also due to be confirmed. The OPEC meets this week to reach consensus on crude production in 2018. China stocks had a meltdown on Thursday. Angela Merkel’s government is struggling and there’s the possibility of a snap German election. The Brexit drama continues.

The markets must discount disagreement between S&P and Moody’s on sovereign ratings. There’s an important change, via ordinance, in the IBC (Insolvency and Bankruptcy Code). Beyond the economics, many traders will sit on the fence until the Gujarat and Himachal election results.

The Q2 results were lumpy in sector contributions and had a positive bias for larger firms. A study by Business Standard of 1,850 listed companies shows overall revenue grew 8.7 per cent year-on-year while net profits declined YoY by 2.6 per cent. The Nifty’s net profits were up by 12 per cent. Those 50 companies accounted for over 80 per cent of the combined net profits of the sample (up from 78 per cent YoY). There have been some cuts to consensus estimates.

Disclaimer: These are personal views of the writer. They do not necessarily reflect the opinion of www.business-standard.com or the Business Standard newspaper