Private banks, NBFCs gain at govt banks' expense

Bonds raised by private firms also show a sharp increase

"graph")

premium

graph

Last Updated : Oct 11 2017 | 4:15 AM IST

As public sector banks (PSBs) go slow in giving credit to industry, private sector banks and non-banking finance companies (NBFCs) have been quick to lend a helping hand.

PSBs have seen their market share in loans to the commercial sector erode from 70.9 per cent in 2014-15 to 64 per cent in 2016-17. Private sector banks have gained 680 basis points to reach 33.1 per cent in the same period.

Compared to banks, whose year-on-year (YoY) credit growth rate was 5.1 per cent in 2016-17, NBFCs registered 13 per cent growth. NBFCs have increased their market share in credit to business from 2 per cent in 2015-16 to 2.8 per cent in 2016-17.

A study released by the Reserve Bank of India (RBI) on Tuesday showed that NBFCs disbursed Rs 84,000 crore of commercial loans in 2015-16, but the segment rose sharply to Rs 1.24 lakh crore in 2016-17, growing the book by 8.8 per cent.

At an aggregate level, the corporate sector seems to be shifting away from the bank loan market to other means of raising funds, such as bonds, equities and private equity funds, an analysis of funding patterns shows.

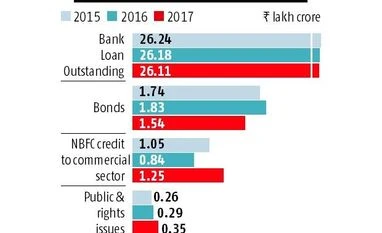

Either because of banks’ unwillingness to lend in the face of a huge bad debt mess or because companies are gaining access to cheaper funds elsewhere, the outstanding loan book to industries (micro, small, medium and large) is shrinking every passing year. The RBI data shows credit outstanding to the industry segment was at Rs 26.24 lakh crore as on August 21, 2015. As on August 19, 2016, the outstanding credit shrank to Rs 26.2 lakh crore and further to Rs 26.11 lakh crore as on August 28 this year.

For this analysis, fund-raising by financial firms was excluded wherever possible.

Meanwhile, the investment intention is showing a mixed trend. According to the Ministry of Commerce data, proposed private investment in calendar 2014 was Rs 4.05 lakh crore, in 2015 it fell to Rs 3.11 lakh crore and then again in 2016, the proposed investment rose to Rs 4.14 lakh crore. Till June 2017, the investment proposals received by the government were to the tune of Rs 2.56 lakh crore.

India Ratings and Research said in a report on Tuesday that over fiscal years 2018-20, growth capex would be muted and overall corporate sector investment would grow by Rs 1 lakh crore, growing at a compound rate of 5-8 per cent, primarily “in the form of maintenance capex”.

“Even if consumption demand picks up, there would be credit supply constraints with regard to providing fresh credit to corporate entities by the banking sector owing to risk aversion and higher recapitalisation needs,” India Ratings said.

However, Credit Suisse has another take on why the loan growth is anaemic, at 6.8 per cent, year on year, as on September 15.

According to Neelkanth Mishra and Prateek Singh of Credit Suisse, “The financial services industry is in a rare and unprecedented position of having a surfeit of capital but not enough demand for it.”

“The problem seems to be demand, not supply,” the duo said, adding, lower rates have not helped stimulate demand. While mortgage loans are not growing, the much larger industry segment is no longer a drag on overall credit, but is seeing no growth even on a weak base, and across sectors.

While the bank numbers have not reflected growth, other means of financing, particularly the bond and private equity markets, remained robust.

The non-financial companies, though, found the best mode of financing in the bond market. In calendar 2015, bonds raised by private non-financial corporate firms totaled at Rs 1.73 lakh crore. This rose to Rs 1.83 lakh crore in calendar 2016 and so far this calendar, firms have raised Rs 1.55 lakh crore. The interest rate in the bond market regularly remained lower than bank lending rates for firms in the past three years. Prabal Banerjee, group CFO of the Bajaj Group, said the difference in rates can be as much as 200-300 basis points for companies with good financial health.

“For good companies, it is a way of refinancing their costly bank loans,” said Banerjee.

According to some experts, this is a clear sign that companies could be leaving banks for other modes of fund raising.

“The way things are headed, I don’t think there will be any top-rated borrowers left on any bank balance sheet. It is a serious issue,” said HSBC India’s head of global markets, Hitendra Dave, in a recent interview with Business Standard.

However, Banerjee said the bank loan market can never be replaced as the bond market is not easy for companies with average to low ratings.

“Companies in the manufacturing sector will necessarily have to tap the bank loan market as they mostly don't have good ratings, and the bond market is not ready to give money for more than three to five years. For project finance, and term loans, banks are the only reliable option so far,” Banerjee said.

Through initial public offerings and rights issues, the corporate sector raised roughly Rs 17,440 crore in 2017 so far, Rs 14,500 crore in 2016 and Rs 13,220 crore in calendar 2015, considering about half of the fund-raising was undertaken by non-financial firms. Issuance to qualified institutional buyers was excluded from this calculation as about 90 per cent of the capital raised was by banks and other financial firms.

Also, at a time when banks shied away from lending, companies found saviours in private equity funds. According to Venture Intelligence, which tracks private equity finances, investments hit an all-time high in 2017 even as the year has three months to go. Calendar to date in September, $17.6 billion equivalent (Rs 1.15 lakh crore) in private equity flowed into the corporate sector, compared with 2016’s $15.55 billion and 2015’s $17.3 billion. However, some of these funds have gone to the financial services and insurance companies too, segregated data for which were not readily available.

Bank loan outstanding as of August for each year; bonds, public & rights issues and private equity data for calendar years 2015 and 2016, and January-September 2017; NBFC data is for financial year ending March. IDFC was included as an NBFC in 2014-15, and in private sector banks the following year; bonds data is excluding NBFCs' debt issuances. Source: RBI, Prime Database, Venture Intelligence