Long-term trend has turned negative

)

The downtrend continued in the markets and a long-term bear market now appears to be odds-on. The global scenario remains volatile. China continues to look like a source of weakness. The US Federal Reserve could perhaps, stem the tide, by making dovish noises at its policy meet next week.

But there doesn't seem to be an immediate, obvious upside apart from short-covering. The foreign institutional investors (FIIs) sold heavily through August and also sold through the first week of September. The rupee is under pressure. The Nifty, the Sensex and other indices are all trading well below their respective 200-Day Moving Averages (200-DMAs). Volumes have been high, which is a dangerous signal when combined with falling prices. Declines also outnumbered advances.

The Nifty-Sensex have recorded successive 52-week lows through the last week. The current low is Nifty 7,545 and the long-term trend is now almost certainly negative, with a pattern of lower lows and the index trading below its own 200-DMA for more than two weeks. Volatility expectations remain high. So, do option premiums in September .

The intermediate trend seems negative as well and so does the short-term trend. To signal an immediate trend reversal, the next peak would ideally move above the 200-DMA (at about 8,250 for an exponential average). The next trough would have to stay above 7,545.

Given the 40-month length of the previous bull market, the bear market could also last a long time. In terms of retraction calculations, there is a Fibonacci retracement level at around Nifty 7,400, which would be a 37 per cent correction of the prior bull market run from a low of 4,531 (December 2011) to a high of 9,119 (March 2015). The next Fibonacci retracement levels of 6,800-7,000 may also be important in terms of sentiment. That's where the index was during the general elections, before this government took power in May 2014.

The rupee has slid below 66.80 versus dollar. If the Fed raises policy rates, a further drop is quite possible. The forex market is liable to stay very volatile with every emerging market currency seeking lower lows versus the dollar in the wake of the yuan devaluation and the euro also witnessing pressure. Information technology and pharmaceutical stocks are potential hedges.

The Bank Nifty has, as always, lost more ground than the Nifty. September is likely to continue to be volatile. A long strangle on the Bank Nifty of long 15,000p (210) and long 17,000c (102) costs 312 (about 0.98 per cent), with the index at 15,800. This could gain handsomely if September remains volatile.

The Nifty's put-call ratios are hovering at neutral levels of 1.01 for both the three-month and one-month series. The call chain for September has peaks at 8,000c, 8,200c, 8,500c despite the fall to below 7,600. The September put chain has an open interest (OI) peak at 7,500p and very high OI at every strike down to 7,000p. Premiums are very high but spreads are reasonable. It is reasonable to seek decent risk:reward ratios at some distance, given the high volatility and implied volatility.

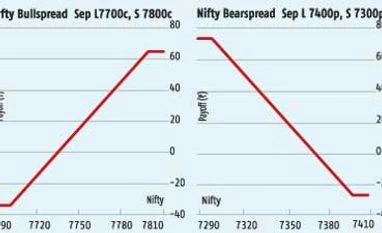

The Nifty traded at 7,558 on Monday. A bullspread of long September 7,700c (109), short 7,800c (73) costs 36 and pays 64 and its struck 140 points from spot. A bearspread of long September 7,400p (111), short 7,300p (85) costs 26 and pays a maximum 74 and this is 160 points away.

Sooner than combining these Nifty spreads to create long-short strangles with an adverse risk:reward ratio, the trader could take the recommended wide long strangle in the Bank Nifty. That will almost certainly return more in the event of a big move.

Don't miss the most important news and views of the day. Get them on our Telegram channel

First Published: Sep 07 2015 | 10:43 PM IST