Street raises a toast to United Spirits

)

USL’s stock, which has done well since October last year after news of its stake sale to Diageo did rounds, is expected to deliver good returns despite the strong run-up and high valuations. The Street remains bullish and expects the company to gain significantly post change of guard to Diageo.

“We expect the deal with Diageo to provide respite to the burgeoning debt and Ebitda margins are likely to improve due to premiumisation, better financial control and price hike in Andhra Pradesh (happened in December 2012 quarter end),” says Abneesh Roy, associate director - institutional equities – research, Edelweiss Securities. Analysts at Motilal Oswal Securities also have a buy rating on USL with a target price of Rs 2,490.

Among the few risks, is imposition of higher taxes on the company’s products.

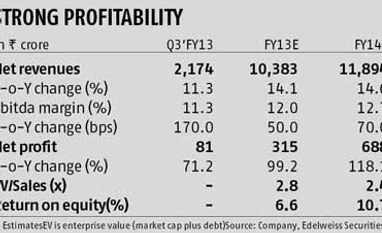

USL’s December quarter standalone results were largely in-line with Street expectations. Strong volume growth of seven per cent (highest since the December 2011 quarter) was largely a function of robust growth (29 per cent) in its premium brands, such as Royal Challenge, Black Dog and Signature. Higher contribution from premium brands, which now forms 25 per cent of overall revenues (21 per cent in the year-ago period), also rubbed off favourably on USL’s Ebitda margins, which increased 170 basis points to 11.3 per cent. The performance could have been better but for Tamil Nadu where preference for local breweries impacted growth in the state and also resulted in 75 per cent capacity utilisation for USL.

On the flip side, declining profitability (Ebitda down 3.6 per cent and profit before tax down 5.8 per cent) of the White & Mackay portfolio (about a fifth of consolidated revenue) was a key negative, and needs to be monitored. Though revenues grew 42.3 per cent to ¤£70 million, higher marketing and overhead expenses impacted operating profits — margins fell 1,700 basis points to 46.8 per cent.

Going forward, USL’s management expects input costs to ease, which coupled with rising premiumisation should lead to further margin expansion (standalone) for the company. This should help earnings grow at a faster pace.

“We expect Ebitda margins to expand by 300 basis points over FY12-FY15, leading to an earnings CAGR of 73 per cent over this period,” says Varun Lohchab, analyst at Religare Capital Markets.

Don't miss the most important news and views of the day. Get them on our Telegram channel

First Published: Feb 07 2013 | 12:54 AM IST