Lead indicators show promise

Wholesale lending rates could fall 50-100 bps before rate cuts

)

The equity markets are at an all-time high, as the market's valuation has expanded. While the government is playing safe on reforms, the market is searching for 'hope' in the key lead indicators, which suggest the worst could be over.

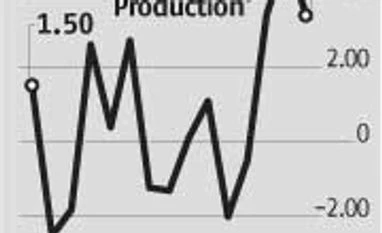

Though the government has not done much to boost economic growth, economists have upgraded expectations for FY15 and FY16. Economic growth is expected to inch closer to six per cent in the second half of FY15, they believe. The upgrades are largely because key indicators are turning positive for the first time since April 2012. Industrial production in the June quarter grew 3.9 per cent, against a contraction of 0.5 per cent in the March quarter. The other indicators economists are tracking closely include loan growth, cash demand, corporate earnings, construction activity and demand for consumer goods and services. Bank of America Merrill Lynch says, “Our lead indicator panel is now sending stronger signals that growth is bottoming out. And, when will we blow ‘All Clear’ once we see lending rates come off to revive demand.” While credit growth has declined to 11.2 per cent on August 8, economists believe loan growth should pick up towards the second half.

Confidence levels have significantly improved after the elections. This is visible in the growth in automobiles and telecom subscribers. Cement volumes have grown 10 per cent in the June quarter, highest in nine quarters, led by a lower base and delayed monsoon. While analysts have not formally upgraded cement volume estimates for FY15, they claim there is an upside risk. The automobile sector saw practically no growth over FY12-14, says Credit Suisse, after some front-loading in FY09-11. It could play catch-up with the structural uptrend and other categories could also benefit.

There's support coming from another unexpected quarter. Higher interest rates are expected to keep investment demand low but the robust flow of capital from foreign investors is expected to cushion the rate impact. If flows continue and the current account deficit stays below $35 billion, India could end FY15 with a balance of payment surplus of $40 billion. With this and loan growth near 15-year lows, Credit Suisse says wholesale funding costs could fall by 50-100 basis points, and even below the repo rate (as in FY04-05), if the Reserve Bank of India does not sterilise these by selling bonds.

Confidence levels have significantly improved after the elections. This is visible in the growth in automobiles and telecom subscribers. Cement volumes have grown 10 per cent in the June quarter, highest in nine quarters, led by a lower base and delayed monsoon. While analysts have not formally upgraded cement volume estimates for FY15, they claim there is an upside risk. The automobile sector saw practically no growth over FY12-14, says Credit Suisse, after some front-loading in FY09-11. It could play catch-up with the structural uptrend and other categories could also benefit.

There's support coming from another unexpected quarter. Higher interest rates are expected to keep investment demand low but the robust flow of capital from foreign investors is expected to cushion the rate impact. If flows continue and the current account deficit stays below $35 billion, India could end FY15 with a balance of payment surplus of $40 billion. With this and loan growth near 15-year lows, Credit Suisse says wholesale funding costs could fall by 50-100 basis points, and even below the repo rate (as in FY04-05), if the Reserve Bank of India does not sterilise these by selling bonds.

Don't miss the most important news and views of the day. Get them on our Telegram channel

First Published: Aug 27 2014 | 9:36 PM IST