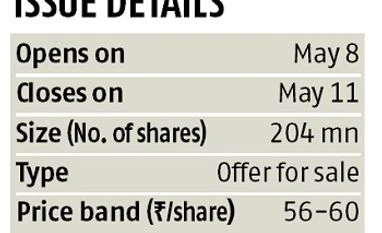

Hudco IPO opens today: Here are the numbers, valuation, financial details

An overall momentum in favour of affordable housing positions the IPO attractively

"graph")

graph

The initial public offering (IPO) of Hudco, formerly known as Housing and Urban Development Corporation, comes at an interesting time, given the government’s interest in housing, especially affordable housing. Nonetheless, the company’s fundamental prospects are equally worthy of mention, including initiatives by Hudco’s management in the past three years to ensure that there is a clear focus in its lending strategy, which in turn will ensure that previous problems of non-performing assets (NPA) do not recur. Overall, while there are a few worms in its financials, there is more on the bright side.

Business operations

Hudco’s primary focus is to lend to state and central government projects pertaining to housing and urban infrastructure. As on December 31, 2016, its loan book stood at Rs 36,386 crore with about 31 per cent being loans to the housing sector and 69 per cent to the infrastructure sector. State governments and their agencies constitute 90 per cent of the loan book.

Under the urban infrastructure lending division, Hudco has 34 per cent exposure to water supply projects, 29 per cent to road projects and 21 per cent to state electricity distribution companies. About 87 per cent of the urban infrastructure loan book is constituted by loans to states, while the share of the private sector is seen at 13 per cent, down from 17 per cent in 2013-14. This is after Hudco decided in 2013 to discontinue lending to the private sector, given the mounting NPAs in loans to private developers.

Financials

As lending to government bodies is Hudco’s core activity, investors should not expect a dramatic year-on-year increase in its loan book or earnings. But what they can be assured of is stable and steady financials (see table). A net interest margin (NIM) at 4.3 per cent for nine-months of FY17 is among the best in the industry.

Hudco taps into tax-free and taxable bonds, deposits, commercial paper, refinancing assistance from the National Housing Board and term loans to meet its funding needs. Government ownership also helps it access long-term loans at low cost. This structure is unlikely to change in the near future. Even if it does, there is ample room for leverage, given Tier I capital of 67 per cent as against the requirement of less than 10 per cent. High capitalisation is because loans to states are backed by guarantees, securities, mortgages or even negative lien. This is why NPAs for state projects are well below 1 per cent. However, impediments in replicating a similar structure with private sector loans have resulted in an overall gross NPA ratio of 6.8 per cent. While efforts are under way to reduce this stress, it may take another 12–18 months before NPAs come down from the current elevated levels. While this is a risk to earnings, once the clean-up is done, return ratios should significantly brighten.

Other risks

A change in the government’s stand on affordable housing may alter the competitiveness of Hudco, which though seems unlikely anytime soon. Likewise, a sharp change in bond yields or an inability to tap the tax-free bonds route may weigh on NIMs. The IPO, which is an offer for sale, will bring the government’s stake in Hudco down to 89.8 per cent. However, to meet the mandatory holding requirement of 75 per cent, follow-on issuances are likely, which can keep the stock price under check.

Valuations

At the upper end of the price band, valuations work out to 1.4x FY16 price-to-book. While there are no near about comparables in the wholesale financing segment, at these valuations Hudco is at a discount to most fast-growing and prominent housing finance companies, such as LIC Housing and HDFC. Most analysts, including Motilal Oswal Securities, IIFL, Antique Stock Broking, Reliance Securities and Axis Capital recommend investors to subscribe to Hudco’s IPO.

Don't miss the most important news and views of the day. Get them on our Telegram channel

First Published: May 08 2017 | 8:53 AM IST