Extra borrowing to put pressure on yields

Nevertheless, yields will rise in reaction to the announcement

"graph")

premium

Last Updated : Dec 30 2017 | 2:29 PM IST

The Reserve Bank of India (RBI) has re-adjusted the last five bond auctions for government finances to Rs 15,000 crore each, from Rs 5,000 crore scheduled earlier, to accommodate Rs 50,000 crore of extra borrowing this financial year.

While the numbers were shared after market hours, bank stocks had earlier reacted negatively in anticipation of what was coming. The market was expecting extra borrowing from the government between Rs 30,000 crore and Rs 50,000 crore. Bond dealers did not believe the last five auctions would remain in the size of Rs 5,000 crore. Usually, the weekly borrowing size is always at least Rs 15,000 crore.

Nevertheless, yields will rise in reaction to the announcement. What confused the market and analysts alike, though, was the accompanying statement from the government, wherein it was stated the treasury bill stock would be reduced by Rs 61,203 crore and borrowing through dated securities would be Rs 50,000 crore.

In the Union Budget announcement, the government had said the net addition, after considering borrowing minus redemptions, through treasury bills, would be Rs 2,002 crore. So far, net collections through t-bills is Rs 86,203 crore. The government said it would reduce this to Rs 25,006 crore.

“The government will thus, between now and March 2018, not be raising any net additional borrowing (t-bills will be run down by Rs 61,203 crore and additional g-sec borrowing will be Rs 50,000 crore),” the government release said.

Confusion prevailed over whether the government meant the net outstanding in t-bills now would be Rs 25,006 crore, which is much higher than Rs 2,002 crore and therefore the additional Rs 23,000 crore should be added to the deficit numbers. The additional dated borrowing of Rs 50,000 crore, too. In that case, the extra borrowing would be Rs 73,000 crore, at par with the buyback of the government of Rs 75,000 crore. Even as the government is freeing resources through cuts in t-bills outstanding, it is actually not scaling back the number to the budgeted Rs 2,002 crore, goes the logic. Bond yields would shoot up in that case.

The alternative explanation is that the government now means the outstanding t-bill stock would be Rs 2,002 crore minus Rs 61,203 crore or minus Rs 59,201 crore of t-bill receipts. In that case, the deficit number doesn’t get affected at all but the maturity does get prolonged, as the t-bill issued in the fourth quarter (gross Rs 1.79 lakh crore) has minimum maturity of 91 days, meaning they mature only in the next financial year.

“In any case, I don’t think the fiscal slippage would be much higher for this fiscal. The implications of this will be felt in the next one,” said Aditi Nayar, chief economist with ratings agency ICRA. In that case, the yields will have less pressure; however, the yields will be under pressure in any case.

“The announcement suggests no incremental borrowings in the remaining part of the financial year but that doesn't mean no alteration in full-year borrowing. These are likely to exert pressure on yields,” said Soumyajit Niyogi, associate director of India Ratings and Research.

The market reacted before the close on buzz that the extra borrowing would come at around Rs 30,000 crore, which would have been at the lower end of expectation. Yields fell three basis points (bps) an hour before the market closed. The extra borrowing being at the higher end of market expectation would mean the 10-year bond yields would readjust back to 7.3 per cent, dealers said. Eventually, these might rise to 7.4 per cent, considering the bond supply would continue, even as space for foreign investors in local bonds have already been filled, said Harihar Krishnamurthy, head of treasury at First Rand Bank.

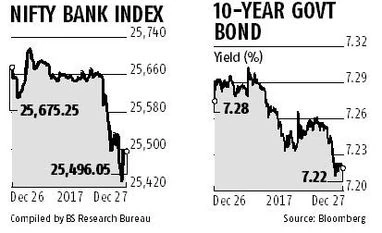

The yield on the 10-year benchmark government security on Wednesday rose to as much as 7.31 per cent in intra-day trade. The security, however, closed near the day’s low of 7.22 per cent, compared to the previous day’s close of 7.27 per cent.

Bond yields have been rising since August, despite a rate cut that month and RBI assurance on liquidity. The yields have risen more than 80 bps points since the last rate cut in August, as the market did not believe there would be more. Bond dealers were also suspicious about the government’s fiscal deficit target numbers, in the face of falling tax and non-tax revenue collection and at a time when dividends from banks and RBI were falling.

“Yields will rise because at the fag-end of rate cycles, any small news point gets accentuated and affects the psyche,” said a bond dealer.

According to Krishnamurthy, bond market sentiment has been hit and the coming Budget will be carefully monitored. “The government’s fiscal stance and RBI’s monetary stance would be carefully watched. It doesn’t look like there is much of a space for the deficit numbers to remain within the target zone. Yields should rise from the present levels, especially after the extra borrowing,” he said.

Banking shares underperformed the market on Wednesday on concerns of additional borrowing by the government. The Bank Nifty index fell 0.7 per cent, the most in three weeks, while the benchmark Nifty index declined 0.4 per cent. Experts said higher borrowing would put pressure on bond yields, which could lead to treasury losses for banks. Also, fiscal pressure could impact the bank recapitalisation plan, feared investors.

Among government-owned banks, Canara and State Bank of India declined the most at 2.1 per cent and 1.2 per cent, respectively. Private lenders ICICI Bank and HDFC Bank fell nearly one per cent each. Of the 12 Bank Nifty constituents, only IDFC Bank managed to close with a slight gain.