StatsGuru: 31-March-2014

Key indicators RBI will consider to decide monetary policy

)

Click on graphic

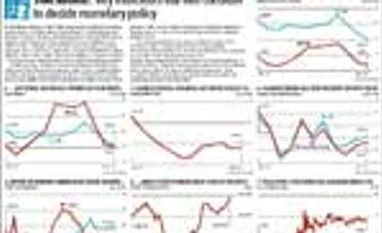

As the Reserve Bank of India (RBI) prepares to revisit its monetary policy stance, it will be aware that inflation is definitely on the decline. As Table 1 shows, both Wholesale Price Index (WPI)-based inflation and Consumer Price Index (CPI)-based inflation have fallen of late - though retail inflation remains high, at around eight per cent. It will note, however, much of the decline in retail inflation stems from a fall in food price inflation, shown in Table 2 - and that might reverse itself in time, without structural reform.

It will also note, however, that manufacturing inflation has lately remained below the three-per-cent mark, indicating tight money is playing a role already. Growth in the industrial sector has, in fact, pretty much been turned off, as Table 4 shows; while growth in the overall Index of Industrial Production has been around zero for a while, manufacturing has shown negative growth on IIP.

The central bank will also see, as Table 5 reveals, that deposit growth is now steadily above credit growth, indicating that investors do not see real interest rates at banks as too low. It will also keep an eye on its foreign-exchange reserves, which have increased recently, as Table 6 shows - buying dollars means there are more rupees in the market, which increases inflationary pressures. And, as Table 7 shows, the yield from government securities has stabilised at below nine per cent.

Don't miss the most important news and views of the day. Get them on our Telegram channel

First Published: Mar 31 2014 | 12:05 AM IST