FCNR golden goose: Great returns on borrowed capital

Foreign banks in rush to raise dollar deposits from NRIs to milk RBI's special window

)

Foreign banks are scrambling to raise dollar deposits from non-resident Indians — even tempting them with loans — to open their foreign currency non-resident (bank), or FCNR (B), deposit accounts in India.

The move comes after the Reserve Bank of India (RBI), as part of its efforts to stem the rupee’s depreciation, opened a special window for swapping FCNR (B) dollar funds of three years or more at a concessional rate and offered various other incentives, including cheap dollar-rupee swap rates.

Observers say this has offered Indians residing abroad an opportunity to increase their income manifold using borrowed capital.

The process, as bankers and market participants explains, begins with a foreign bank requesting a non-resident to open a FCNR (B) deposit account with its India unit. The bank immediately offers the customer a loan against this deposit. The customer uses the loan to create another FCNR (B) deposit account, against which he is again given a loan. The process is repeated eight to 10 times. The customer benefits as he earns more interest on FCNR (B) deposits than he pays on loans against those.

Some of the Indian banks with foreign branches have also approached their non-resident customers to raise FCNR (B) deposits, but observers say these lenders are not as aggressive as their foreign rivals.

Industry analysts say, using this mechanism, non-resident Indians (NRIs) can make a net return that is significantly higher than the interest rates offered on deposits in developed markets like the US. The returns would easily lure NRIs. According to some estimates, by putting up just 10 per cent of the deposits, the client effectively makes between 18 and 21 per cent on the dollars.

The process, however, has raised concerns of systemic risk.

“The 2008-09 crisis was triggered by over-leveraging. We are again seeing foreign banks encouraging leveraging. There are reports that lenders are offering NRIs upfront loans against FCNR (B) deposits and repeating the process. Such leveraged money can leave as abruptly as it comes in, thereby increasing systemic risk,” Ajit Ranade, chief economist of Aditya Birla Group, says.

On September 4, 2013, in an almost desperate move to arrest the slide the rupee, RBI had announced a window for swapping FCNR (B) dollar funds, mobilised for a period of at least three years, at a fixed rate of 3.5 per cent a year for the duration of the deposit. The scheme, the central bank had said, would remain operational until November 30, 2013.

In other words, the banking regulator is now permitting lenders to convert three-year FCNR (B) dollar deposits into rupees at 3.5 per cent, even though the swap cost, considering the recent rupee-dollar forward rates, is estimated to be more than six per cent. This has encouraged banks to mobilise FCNR (B) dollar deposits, as they can reduce their cost of fund by at least 250 basis points using this window.

“It is a win-win situation for all. The interest rates offered to non-residents on three-year FCNR (B) deposits in India are significantly more than the current dollar swap rate of 80 basis points a year for a comparable tenure. Banks will benefit, as they will have access to low-cost funds. And, ultimately, this will increase dollar flows into India,” Param Sarma, director and chief executive of NSP Treasury Risk Management Services, says.

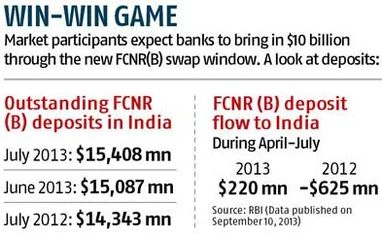

Market participants expect banks to bring in over $10 billion through this route which will probably avoid the need for an immediate sovereign bond issue by the government.

“The swap window was necessitated by a sharp depreciation in the rupee and need to bridge the current account gap. There was a need for one large chunk of dollar inflow, which probably led to the introduction of this scheme. However, it is a subsidy, assuming the rupee-dollar swap cost is currently over six per cent. This subsidy will have to be borne by the country,” says Mecklai Financial Deputy CEO Partha Bhattacharyya.

Some industry analysts believe the subsidy burden on Indian taxpayers because of this move might be as high as Rs 2,000 crore a year, assuming banks bring in $10 billion of FCNR (B) deposits.

“We discontinued FCNR (A) deposits since we did not want to bear the entire currency risk, and these deposits also violated IMF (International Monetary Fund) conditions. But by allowing swap at a concessional rate of 3.5 per cent for FCNR (B), we are going back to the FCNR (A) regime, at least partly. I believe, we should be explicit in saying what would be the estimated cost of this subsidy, since the deposits might run up to five years,” Ranade adds.

Don't miss the most important news and views of the day. Get them on our Telegram channel

First Published: Sep 26 2013 | 12:57 AM IST