Kunal Kumar Kundu: A change for revival

India's growth model needs to change from being consumption-driven to investment-driven in order to revive the economy

)

Growth in India's gross domestic product (GDP) for the fourth quarter of FY14 confirmed the economy was in stagflation, as it faced one of its worst slowdowns over the past 26 years. However, we believe that India's economy is bottoming out, although recovery will be slow. The expectation of mild recovery during the current year is based on the assumption that the formation of one of the most stable governments in India over the past three decades would ensure the removal of policy paralysis afflicting the economy. This will engender an investment-led recovery as business sentiment perks up.

Anecdotal evidence suggests many investors were waiting on the sidelines, especially during the final stages of the previous government's tenure, as political uncertainty rose, policy paralysis gripped the country and business confidence plummeted. However, with the formation of a stable government at the Centre, the pall of gloom seems to have been lifted and business confidence is returning, albeit slowly as investors are keenly awaiting policy moves from the government. Nevertheless, history suggests that the removal of uncertainty can act as a catalyst that can spur economic growth.

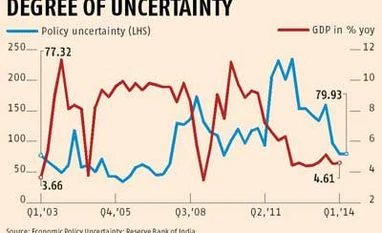

To ascertain how policy-level uncertainty has changed over a period of time, we consider the Economic Policy Uncertainty (EPU) index introduced by Scott Baker, Nicholas Bloom and Steven Davis. To measure policy-related economic uncertainty for India, they have constructed an index based on newspaper articles regarding policy uncertainty, with certain sets of key words. A high EPU score indicates a higher degree of uncertainty, while a low EPU score indicates an increasing level of certainty. We then plot the EPU index with the GDP growth data and, not surprisingly, we see higher level of GDP growth coinciding with stable policy environment.

According to the data, India has never had such a prolonged period of policy uncertainty, as the latest episode suggests, and this period also coincides with sustained growth slowdown. Now, with policy uncertainty gradually inching down, GDP growth has likely bottomed out. In fact, the index for Q2 2014 is the lowest since Q4 2007, indicating a much greater environment of policy certainty.

The fact is, India's growth model needs to change from being consumption-driven to investment-driven. The recent slowdown in economic growth and spike in inflation can largely be attributed to the sharp fall in fixed capital formation in the economy, thereby exacerbating the structural constraints. Falling policy uncertainty and concomitant improvement in business sentiment would likely bring about a revival in investment in the economy.

Although an increasingly certain policy environment, improving business sentiment and low-base effect will propel the economy up to and beyond the five-per cent growth rate mark, all eyes are now on government actions during the run-up to the forthcoming Budget. Thus far, the new government has been making all the right noises - economically speaking, that is. However, implementation remains the key. Even if the government is able to carry out reform measures according to our expectations, the current year's growth will still look anaemic (given the past trend). The result of the actions taken will slowly manifest itself from next year onward. Between FY15 and FY19, we expect the Indian economy to grow on an average by 6.3 per cent year-on-year per year.

Tailpiece: Although the bottoming out of the economy bodes well for the rupee, substantial portfolio inflows on the back of high expectation while ignoring the potential inflationary impact of failed monsoons and the Iraq turmoil is a bit alarming. Hope need not necessarily be a good investment strategy.

The writer is vice-president and India economist, Societe Generale.

These views are personal

Disclaimer: These are personal views of the writer. They do not necessarily reflect the opinion of www.business-standard.com or the Business Standard newspaper

Don't miss the most important news and views of the day. Get them on our Telegram channel

First Published: Jul 06 2014 | 9:48 PM IST